1 No-Brainer Artificial Intelligence (AI) Stock to Buy With $30 and Hold for 10 Years

The artificial intelligence (AI) opportunity has never been greater for this trailblazing company.

Artificial intelligence (AI) is relatively new for most companies, but not for C3.ai (AI 3.50%). It has developed the technology since 2009, and it was one of the first enterprise software providers in the fast-growing AI industry.

Today, businesses across 19 industries use C3.ai to accelerate their adoption of AI, and the company’s revenue growth is accelerating as demand soars.

C3.ai stock currently trades at $25.90, but the proliferation of AI could send it significantly higher over the long term. Here’s why investors with spare cash — money they don’t need for immediate expenses — might want to allocate at least $30 to this opportunity.

Image source: C3.ai.

A unique play in the enterprise AI industry

Cloud software giants like Amazon and Microsoft have become synonymous with AI because they offer businesses a choice of hundreds of ready-made large language models (LLMs) that they can use to build their own applications.

C3.ai’s strategy is a little different. It provides over 40 turnkey AI applications that businesses can plug right into their operations. Plus C3.ai can customize them on request to meet specific needs. For example, manufacturers use C3.ai to forecast revenue, manage costs, and even predict equipment failures to reduce potential downtime.

Similarly, oil and gas giant Shell uses C3.ai’s applications to monitor thousands of pieces of equipment so it knows when to conduct preventative maintenance, because failures can be catastrophic — not only for the company’s bottom line, but also for the environment. C3.ai’s Real Time Production Optimization software also helps Shell optimize pressure, temperature, and flow rates at its liquefied natural gas plants, which leads to a substantial reduction in carbon emissions.

During the recent fiscal 2024 fourth quarter (ended April 30), C3.ai had 487 customer engagements, which was a 70% increase from the year-ago period. It closed 115 deals through its partnership network alone, which includes tech giants like Amazon and Microsoft, which offer C3.ai’s applications to their customers in the cloud.

It’s a win-win for all parties — C3.ai gains access to a much larger potential customer base, and its partners benefit from having more AI options on their platforms to satisfy their enterprise customers.

C3.ai’s revenue continues to accelerate

Two years ago, C3.ai changed its revenue model to fuel long-term growth. It previously billed customers on a subscription basis, which required lengthy negotiations on contract duration and pricing. Now it uses a consumption model instead so businesses can come and go as they please and only pay for what they use, which creates a smoother and faster onboarding process.

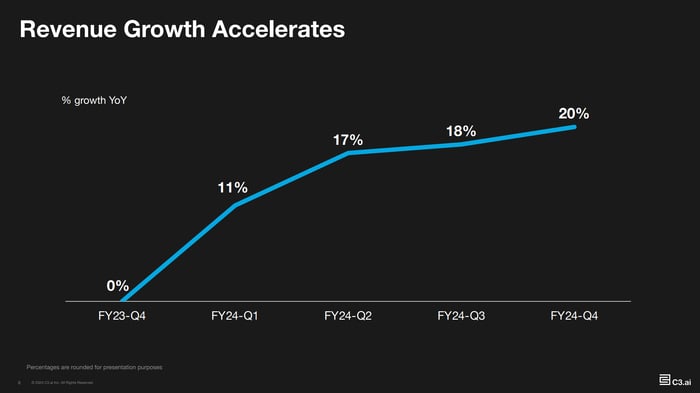

C3.ai warned investors this would lead to a temporary slowdown in its revenue growth while it converted its existing customers to the new model, because it takes time to scale up consumption. In the third quarter of fiscal 2023 (ended Jan. 31, 2023), the company’s revenue actually shrank 4% on a year-over-year basis.

But since then, and true to management’s forecast, C3.ai’s revenue growth has convincingly accelerated:

Image source: C3.ai.

Revenue came in at $86.6 million during Q4, which was a record high, and the 20% growth rate was the fastest in almost two years. The company’s forecast for the first quarter of fiscal 2025 (ending July 31) suggests growth could accelerate even further to 23%.

Why C3.ai stock is a no-brainer buy for the long-term

First, it’s important to highlight that C3.ai continues to lose money. Its net loss came in at $72.9 million during Q4, which was an increase from the year-ago period as the company spent more money on its operating costs (mainly marketing) to drive sales. On a non-GAAP basis, which strips out one-off and non-cash expenses like stock-based compensation, C3.ai’s loss was $14 million, which is a little more palatable.

The company has $750.3 million in cash, equivalents, and marketable securities on its balance sheet, so it can afford to sustain its losses for the foreseeable future, but it will eventually have to prove to investors it can generate a profit to accompany its accelerating revenue growth.

On the other hand, Wall Street’s forecasts suggest AI could add anywhere between $7 trillion and $200 trillion to the global economy in the coming decade. Capturing as much of that value as possible could drive substantial long-term rewards for investors, so it isn’t necessarily a bad thing that C3.ai foregoes profitability in the short run in favor of spending aggressively to acquire customers.

C3.ai stock hit an all-time high of $161 shortly after going public in 2020, so its current price of $25.90 represents an 83% decline. To be clear, the company’s valuation was completely irrational back then, but it has done nothing but grow its revenue and its customer base ever since. Plus, its opportunity in the AI space has never been greater.

Therefore, this could be a great opportunity for investors to buy into C3.ai with the intention of holding for the next decade as the AI story unfolds.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon and Microsoft. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.