Contractor’s Corner: Radiance Solar

The solar industry often talks about ways to cut the soft costs of running a business — the behind-the-scenes project management software, training processes and data analytics that keep projects on schedule and up to quality. But one EPC says now is instead the time for investment into these areas to meet IRA requirements and give project owners peace of mind.

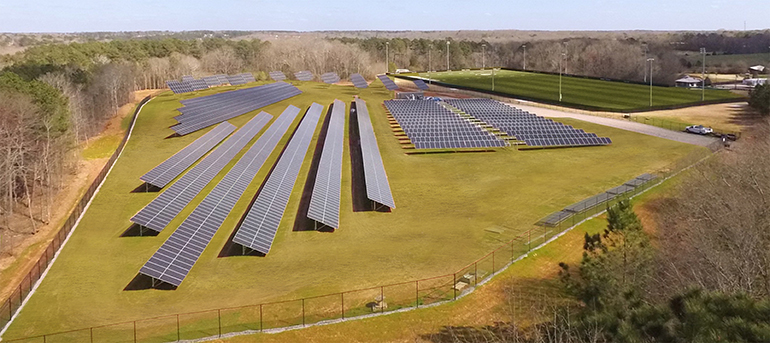

Radiance Solar is based in Georgia, but works on distributed generation and C&I projects across the country. In this edition of our Contractor’s Corner series, we talk to CEO Steve Newby about the company’s commitment to using data to improve workflows and keep projects running as promised.

How does your company stand out from competitors?

How does your company stand out from competitors?

Radiance Solar’s strategy is to deliver utility-scale service and efficiency to the distributed generation market and to do it nationwide. This requires a high level of service from engineering and design, a full safety department, a quality control process and area, highly internally trained construction teams, through to our own commissioning team. We do all of this with our own people and again, we do it for projects across the country. We’re able to bring highly skilled labor to bear in multiple projects across the DG and C&I space.

We’re looking for partners that appreciate our safety, quality and value, and that want us to execute multiple project portfolios in varying geographic areas. We are well-capitalized and have invested to be able to execute this strategy. We see this as a big differentiating factor that will become even more important as the industry continues to become more sophisticated in how it manages the large buildout we all have to accomplish. Finally, we use data analytics as the backbone of our company. We have a team that takes daily field-level data and analyzes it across all projects, systems and geographic locations. We believe we lead the industry in this area and it gives us a significant advantage when discussing with customers their execution strategy on project portfolios.

Has the IRA changed the way you do business, and if so, how?

The IRA has changed the EPC world significantly due to the reporting needed and the training related to the apprenticeship programs. We were early movers here and applied for and received our Dept. of Labor certification early last year. We also have invested heavily in our internal resources to be able to provide the compliance necessary for the IRA. We now have our own internal training area and apprenticeship areas for mechanical, electrical and our O&M groups. This was a big investment on our part. We are seeing IRA compliance really cause a lot of scrambling across the industry for both big and small operators as companies try to catch up on compliance. We actually have already been audited by the DOL and passed with flying colors, which is a real testament to the effort of our team members.

What’s one way you’ve cut soft costs at your company?

What’s one way you’ve cut soft costs at your company?

We have actually had to invest in this area given our significant growth and the needs demanded by the industry (e.g. IRA compliance). Sophisticated clients are very interested in your back-office capabilities and rightfully so as we believe this is an area of increased risk due to the recent regulation. On the engineering front, we are able to capture higher efficiencies because we self-perform our work and this allows our engineering team to work closely with our construction teams on optimizing design.

What solar technology improvement has made installations easier or better and how?

We’re still a very manual industry on the construction piece of our business. There have been some technological improvements on the civil side, with post installations and racking install, but they have been fairly marginal to our efforts. I do think we are going to see more on the engineering piece of the business. We believe AI will begin to make some real headway in that area.

The biggest mover for Radiance is our ability to use data analytics in evaluating our production rates in the field. We have a team that is tasked with using our field data to accomplish a few things for us. Estimating and pricing projects more effectively, providing value-added feedback to our customers on various factors that affect price, and ultimately helping us be more efficient in our installations. As one of the largest DG EPC’s in the country, we have a lot of data across a lot of geographic areas and systems that feed into our analysis. As I mentioned earlier, we believe this work differentiates us from the competition.

What’s your view of the future of the U.S. solar + storage industry?

First, what an exciting time to be in the industry. On the macro level, I think we are at the beginning of a multi-generational change in our domestic energy economy. Electrification is obviously occurring and solar has proven to be the most economical renewable choice. I also think we are early on the distributed generation growth curve. The focus, due to sheer MW added, tends to be on utility-scale installations, but you are going to see a massive increase in DG across the country as we realize, due to a lot of factors, it is better to produce power closer to where we use power.

For batteries, they are a game-changer across the solar space as they will lead the way for solar to become baseload generation. Again, the utility-scale area is leading on the battery front, but there will be, and we are discussing this at length with our C&I customers, significant DG and C&I battery deployment over the next decade. Finally, I think technology gains will really play a huge role for both solar and storage and we need it to continue to bring costs down in the industry.

Needed to accomplish all of this is capital, both financial and human capital. I’m still amazed at how poorly the solar industry is capitalized. All of the private capital that is focused on the space has mostly been focused on the developer/asset owner side or, to some extent, the front-end product side. It has not made its way yet to the service side, e.g., those that enable the installation of all of this solar and BESS. It is just starting to and I think that will significantly increase over the coming years as private capital providers realize the risk/return opportunity in this “service” piece of the industry is attractive. Human capital worries me as much, if not more than financial capital. Skilled labor in this industry, and the country overall, is at a very high premium. We will need a massive shift in labor allocation from other industries to the renewable space to accomplish our goals. This is across both white-collar and blue-collar jobs.