Fintech Thrives Post-COVID-19 with Customer Growth Exceeding 50% – Fintech Schweiz Digital Finance News

Post-COVID-19, the global fintech industry maintained its growth trajectory, driven by both increased consumer interest in fintech offerings and improved accessibility to digital financial services.

Findings from a study conducted by the Cambridge Centre for Alternative Finance (CCAF) and the World Economic Forum (WEF) unveiled that the fintech sector experienced robust customer uptake after the pandemic, achieving an average annual growth rate exceeding 50% across most major sectors from 2020 to 2022.

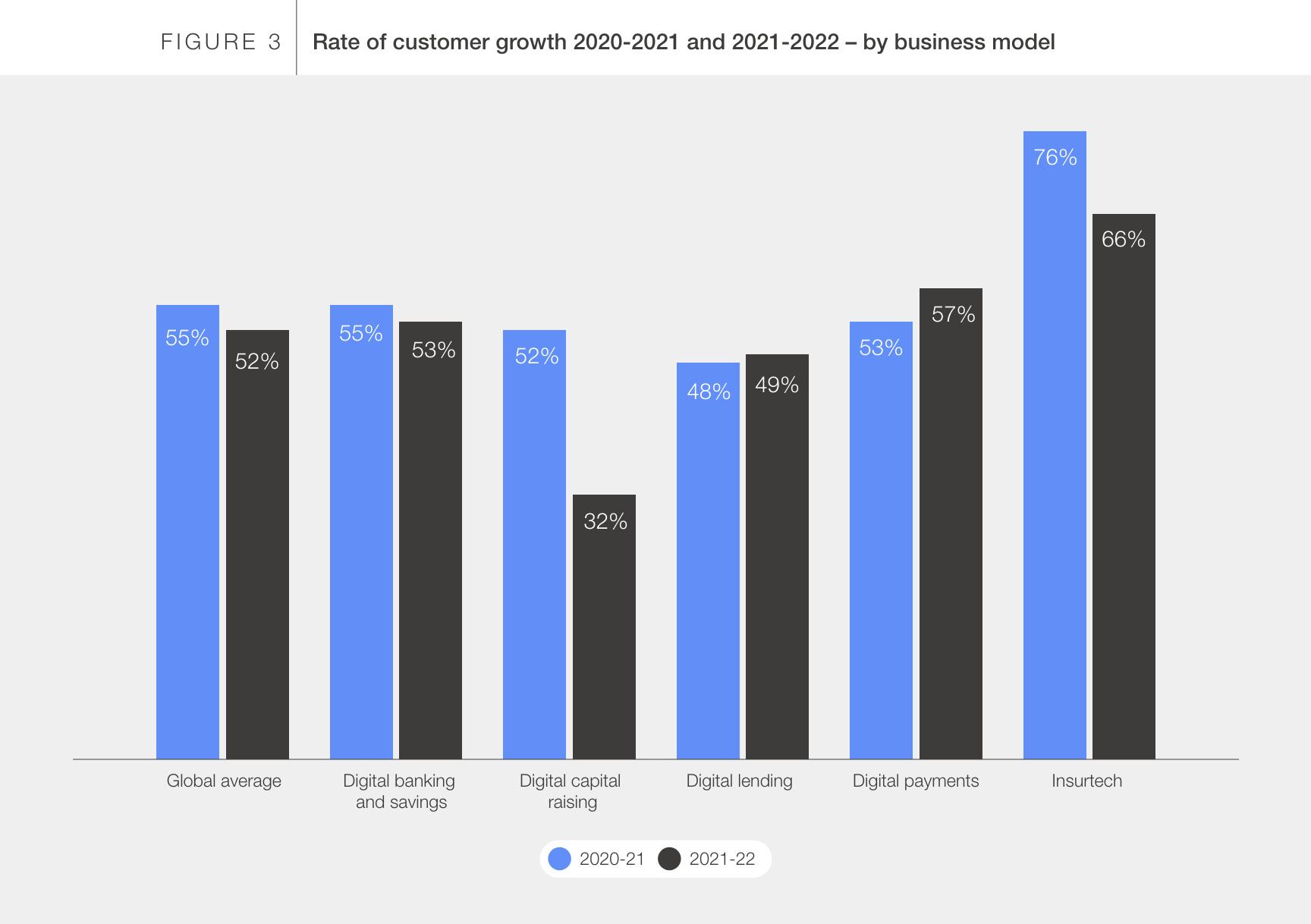

The survey, which polled over 200 fintech companies across five retail-facing industry verticals and six regions, found that fintech companies continued to expand after COVID-19. Except for digital capital raising, which witnessed a significant decrease linked to a challenging environment and rising interest rates, all verticals experienced robust year-on-year (YoY) customer growth rates since 2020.

Notably, insurtech recorded remarkable growth, particularly between 2020 and 2021 (-76%), but experienced a slight decline between 2021 and 2022 (-66%). That drop is being largely attributed to the disproportionate impact of COVID-19 on insurtech in emerging markets and developing economies (EMDEs) where higher value claims, higher numbers of claims and a greater number of insurance policy lapses were observed. Digital payments also showed continued growth, rising slightly between 2021 and 2022 from 53% to 57% and reflecting the continued growth catalyzed during the COVID-19 pandemic.

Rate of customer growth 2020-21 and 2021-22 – by business model, Source: The Future of Global Fintech: Towards Resilient and Inclusive Growth, Cambridge Centre for Alternative Finance and the World Economic Forum, Jan 2024

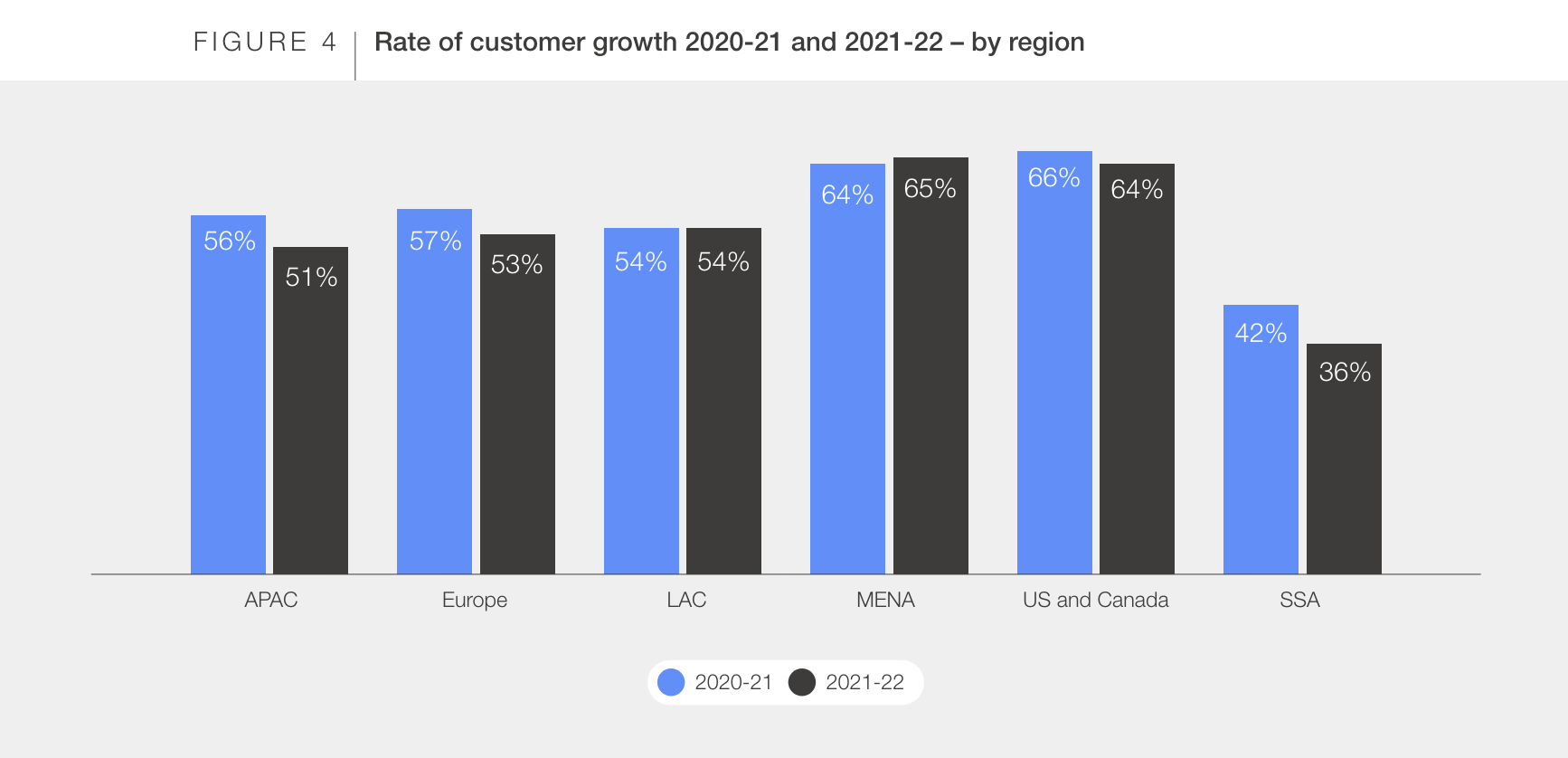

Robust customer growth was observed across various regions, except in Sub-Saharan Africa (SSA), where rates were comparatively lower at 42% between 2020 and 2021 and then at 36% between 2021 and 2022 likely due to infrastructure challenges exacerbated during the pandemic. North America and the Middle East and North Africa (MENA) regions emerged as leaders in customer growth, driven by increasing digitization and structured regulations regarding digital payment methods, banking and credits.

Results of the study also reveal that consumer demand (51%) was the main driver of growth, a trend which is consistent across all regions.

Rate of customer growth 2020-21 and 2021-22 – by region, Source: The Future of Global Fintech: Towards Resilient and Inclusive Growth, Cambridge Centre for Alternative Finance and the World Economic Forum, Jan 2024

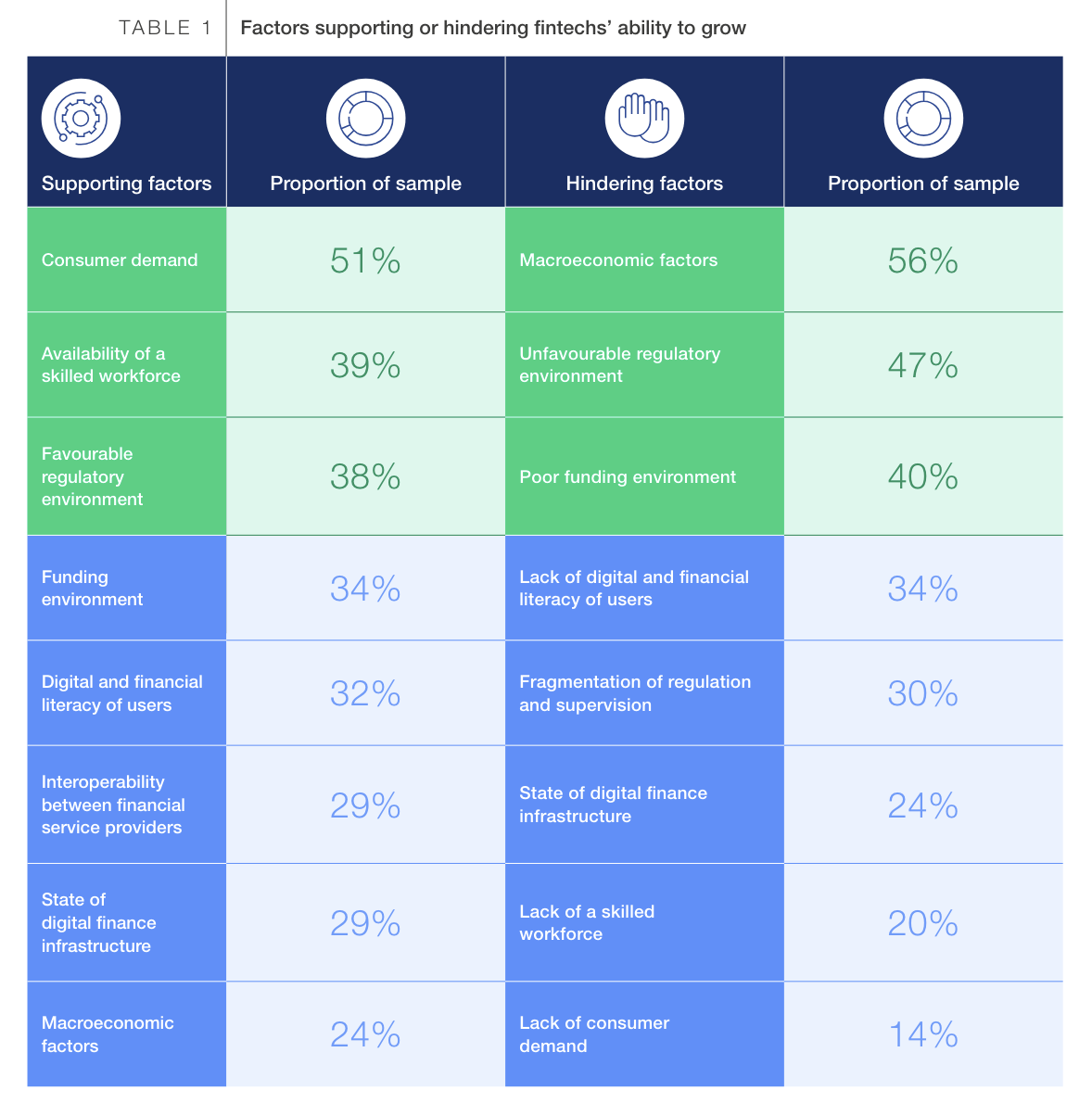

Challenges faced by fintech companies

Despite the positive growth trends, fintech companies are also encountering challenges. Macroeconomic factors, an unfavorable regulatory environment and poor funding environment were identified as the major growth hindering factors, noted by 56%, 47% and 40% of respondents, respectively, amid global inflation and interest rates across the globe.

Interestingly, while challenges varied, regulatory concerns were consistently ranked among the top three factors impacting fintech growth, reinforcing how critical regulation is for fintech growth.

Factors supporting or hindering fintechs’ ability to grow, Source: The Future of Global Fintech: Towards Resilient and Inclusive Growth, Cambridge Centre for Alternative Finance and the World Economic Forum, Jan 2024

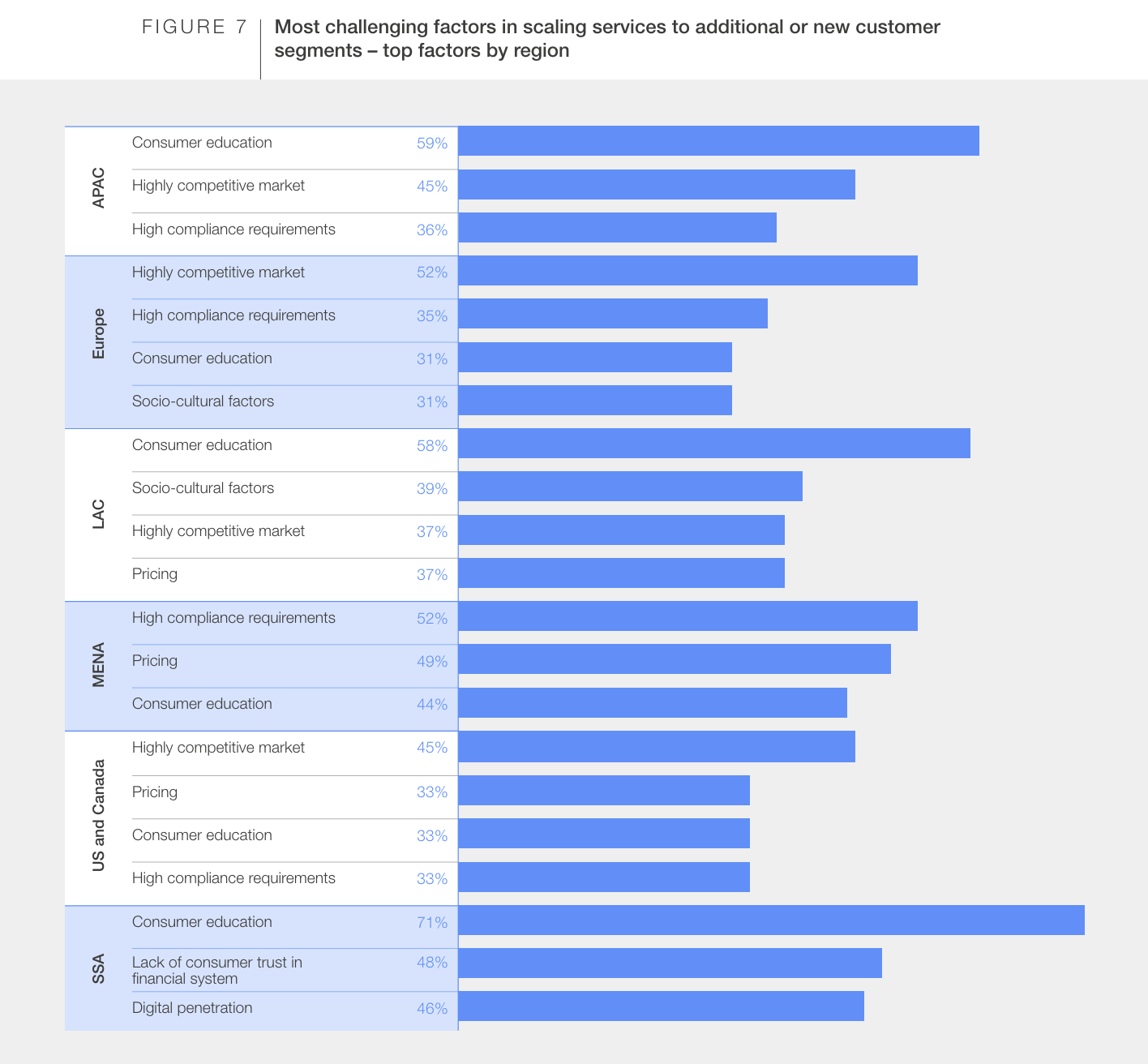

Regionally, fintech companies faced different challenges, suggesting regional variations. European (52%) and North American (45%) fintech companies cited a highly competitive market as their primary challenge to scaling their services to additional or new customer sectors, while those in the MENA region emphasized high compliance requirements (52%). In Asia-Pacific (APAC), fintech companies identified consumer education as their most prevalent challenge (59%), followed by a highly competitive market (45%) and high compliance requirements (36%).

Most challenging factors in scaling services to additional or new customer segments – top factors by region, Source: The Future of Global Fintech: Towards Resilient and Inclusive Growth, Cambridge Centre for Alternative Finance and the World Economic Forum, Jan 2024

Advancing financial inclusion

Results of the study also underscore the role of fintech in advancing financial inclusion. Globally, female, low-income and rural or remotely-located customers constituted a substantial portion of fintech customer bases, averaging 39%, 40% and 27%, while contributing 39%, 26% and 31% of total transaction values, respectively. This trend was consistent across advanced economies (AEs) and EMDEs with small disparities.

Regionally, fintech companies in SSA and MENA recorded the highest proportions of low-income and rural or remotely located customers, with a 47% and 46% representation for low-income customers, as well as 34% and 32% for rural or remote customer segments, respectively.

MENA also led in challenging gender biases, with females constituting 45% of fintech companies’ total customer base, followed closely by APAC and North America at 42% and 41%, respectively. Female MENA customers also contributed nine percentage points more to transaction values than their customer base representation and accounted for 54% of the overall transaction values. In contrast, European fintech companies reported the lowest proportion of female transaction values, at 28%.

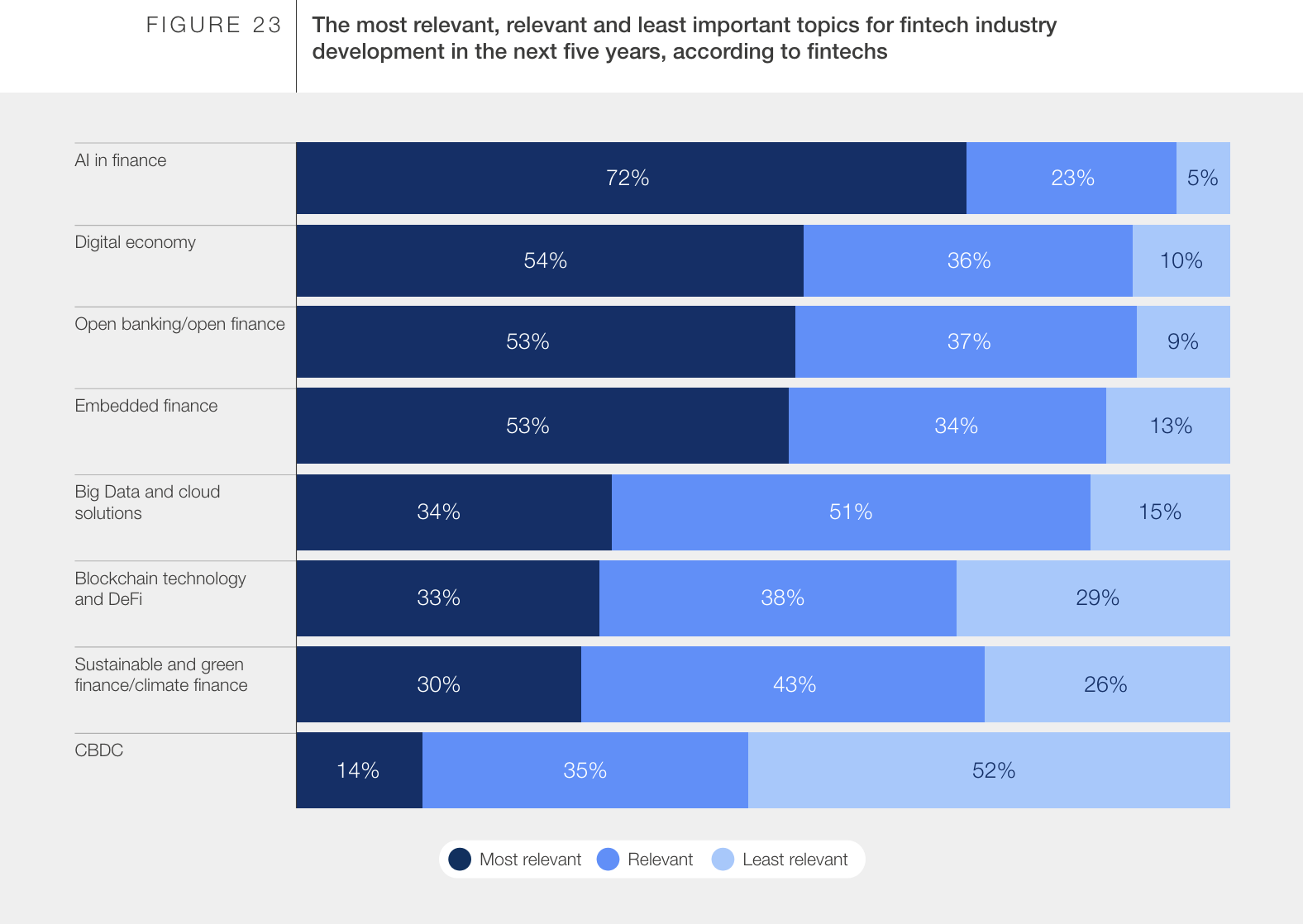

AI, the digital economy and embedded finance as the sector’s biggest trends

Looking ahead, fintech companies identified artificial intelligence (AI) as the most relevant topic for the industry’s development over the next five years. Nearly all verticals acknowledged the significance of AI to bring changes to business models, customer engagement and regulatory frameworks.

Embedded finance, the digital economy and open banking were all nearly tied as the second most relevant factors (53-54%). Surveyed companies said they expected the use of digital platforms to continue to grow, which would ultimately drive the digital economy and, in turn, the rise of embedded finance products. Finally, open banking and open finance are projected to play a critical role in enabling data sharing at scale with customer consent, fueling further innovations in business models and new products.

The most relevant, relevant and least important topics for fintech industry development in the next five years, according to fintech companies, Source: The Future of Global Fintech: Towards Resilient and Inclusive Growth, Cambridge Centre for Alternative Finance and the World Economic Forum, Jan 2024

Featured image credit: Edited from freepik