Global electric vehicle demand raises concerns about battery cell carbon footprint

By a wide margin 2023 was the hottest year on record — and

scientists warn that the weather could only get warmer.

Amid escalating global temperatures and extreme weather events,

the automotive industry faces increasing pressure to reduce

emissions. Rising worldwide demand for battery electric vehicles is

expected to alleviate some climate change effects, but it’s little

respite. Inherent risks and complexities across the vehicle’s life

cycle make realizing their true environmental impact

challenging.

Decarbonization in the mobility sector is now a matter of

necessity. As wildfires, heatwaves, water stress, and hurricanes

become more frequent, they cause ecological and social disruptions

and expose companies’ assets to physical risk. The transportation

sector accounts for a quarter of global greenhouse gas emissions

and is receiving a solid push from government action and regulatory

frameworks to pivot toward sustainability.

Global initiatives such as the Paris Agreement 2015, which aims

to limit global warming to 1.5°C above pre-industrial levels by

2050, have set a clear precedent. Fifteen countries have already

signed net-zero regulations into law, while another 50 countries

have pledged to carbon-neutral targets. The financial sector

displays similar commitments with central banks and stock exchanges

integrating environmental, social, and governance (ESG)

considerations into their reporting and operating requirements.

At the heart of the automotive industry’s journey to

sustainability is the EV revolution. Once a niche market, EVs are

now seen as a critical component of the decarbonization strategy.

However, the transition to electric mobility faces environmental

concerns and sustainability challenges, particularly regarding the

production and lifecycle of EV batteries.

The carbon footprint of an electric vehicle is not confined to

its tailpipe emissions—non-existent in EVs—but is

intricately linked to its battery. The production phase of battery

cells, which involves extracting and processing minerals like

lithium, nickel, and cobalt, is particularly energy intensive. For

example, the cathode and anode materials alone constitute about 72%

of the total emissions from battery production. This aspect is

concerning as it represents a significant portion of the vehicle’s

overall environmental impact.

To further complicate the matter, there are difficulties in

assessing the carbon footprint of EV batteries. The boundaries of

carbon footprint — whether cradle-to-gate, cradle-to-grave, or

well-to-wheel — significantly influence the results and

interpretations of these assessments. Different boundaries in

calculations can lead to varying conclusions about where to make

the most impactful emissions reductions, affecting everything from

consumer choices to regulatory policies.

The United Nations, European Union and other major countries are

attempting to establish globally recognized standards and provide

much-needed consistency in carbon footprint calculations. While

this homogenization remains a work in progress, automakers,

regulators, and manufacturers must increase their efforts to

mitigate carbon emissions from BEVs across the value chain.

S&P Global Mobility’s High Voltage Battery Forecast projects

a 24% compound annual growth rate (CAGR) for global demand for

electric vehicles, from 750 GWh in 2023 to over 3400 GWh by 2030.

With this surge in demand for EVs, the automotive industry faces a

dual challenge. Not only does it need to ramp up production to meet

this demand, but it must also ensure that this expansion does not

come at an unsustainable environmental cost. Companies such as

Tesla, BYD, and General Motors aggressively pursue carbon

neutrality, integrating advanced technologies and renewable energy

sources into their production processes to reduce emissions.

The scale of emissions from batteries by 2030 is estimated to be

equivalent to the carbon footprint of 39 million people globally,

reinforcing the need for aggressive carbon reduction strategies

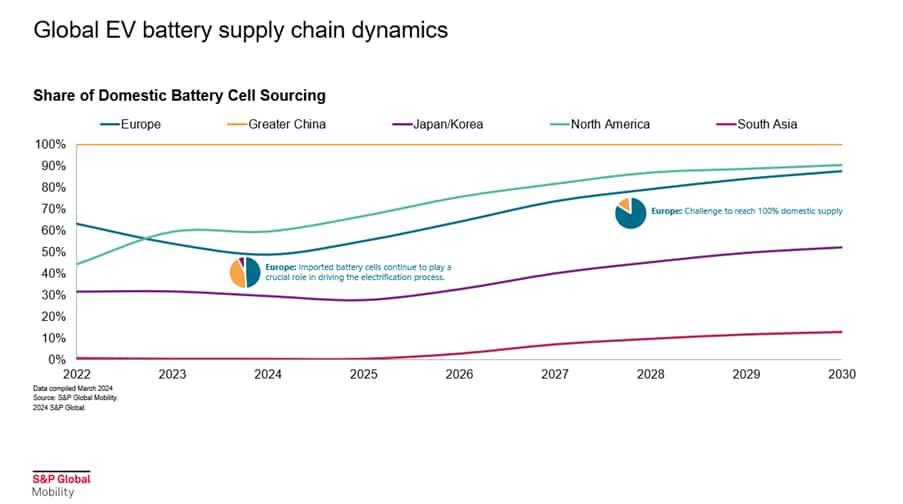

across the battery production lifecycle. Europe is leading the way

with stringent regulations that push for lower carbon footprints in

battery production, which may slow their progress towards becoming

fully self-reliant on domestic supply.

In contrast, China, as a significant battery producer and

exporter, now faces the challenge of reducing its higher carbon

footprint to meet these European standards. With emissions per kWh

of cell manufacturing measured at about 17 kilograms of

CO2 in 2022, China is focusing on reducing this to

sub-10 levels by 2030 through electrification of gigafactories and

investing in provinces with abundant hydroelectricity.

Decarbonizing cathode and anode material production is also

critical, given their significant contribution to the overall

carbon footprint. Together, these changes are setting a precedent

that could define the future of automotive manufacturing

worldwide.

Moreover, the entire supply chain, from mine to market, is under

scrutiny for its environmental impact. The concept of “scope

emissions,” which categorizes emissions into direct, indirect, and

supply chain categories, is helping companies identify and mitigate

their environmental impacts. Using renewable energy in battery

production and adopting carbon-neutral shipping practices are

becoming increasingly common. Such practices are examples of

innovations in supply chain management.

The push for decarbonization is also reshaping consumer

expectations. Today’s consumers are more environmentally conscious,

often willing to pay a premium for sustainably produced goods. This

shift is influencing the automotive sector and the broader

manufacturing landscape as companies across industries strive to

align themselves with their customers’ values.

However, achieving true sustainability in the automotive sector

requires more than clean manufacturing processes. It necessitates a

holistic approach considering the vehicle’s entire lifecycle, from

design and production to end-of-life recycling. The future of

mobility, therefore, lies not only in electrification but in a

comprehensive rethinking of how vehicles are made and used.

As the industry navigates these complex challenges, the role of

international cooperation and technological innovation becomes

increasingly apparent. The journey towards a sustainable automotive

sector is not a solo race but a collective effort that spans

continents and industries. With the right mix of policy support,

corporate governance, and consumer engagement, the goal of a

carbon-neutral mobility sector will be within reach.

This article is part of a series featuring highlights from

S&P Global Mobility’s 2024 Solutions Webinar Series. Objective

Assessment of Battery Cell Contributions to Carbon Footprint

webinar occurred on April 11, 2024.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.