Here’s My Top Artificial Intelligence (AI) Stock to Buy and Hold

Stock to Buy and Hold")

Artificial intelligence (AI) is set to transform multiple industries ranging from smartphones to personal computers, automotive, digital advertising, and cloud computing. Investors should look for potential AI winners in these niches as they could deliver healthy gains on the stock market.

The cloud AI market, for instance, is forecasted to clock annual growth of more than 32% through 2029, according to Mordor Intelligence, generating $274 billion in annual revenue at the end of the forecast period. Major cloud computing providers such as Microsoft and Amazon are some of the names that could help investors capitalize on this tremendous opportunity.

However, I’d like to take a closer look at DigitalOcean (NYSE: DOCN), a cloud company that recently released its quarterly results and suggests that AI-related demand is going to exceed supply. Let’s look at the reasons DigitalOcean could turn out to be a top AI stock in the long run.

The demand for DigitalOcean’s AI-focused services is growing

DigitalOcean released its first-quarter results on May 10, and its revenue and earnings were well ahead of analysts’ expectations. The company’s revenue increased 12% year over year to $185 million, exceeding the $182.6 million consensus estimate. DigitalOcean’s adjusted earnings, meanwhile, shot up just over 50% to $0.43 per share, exceeding the consensus estimate of $0.38 per share.

What’s more, DigitalOcean management has raised the lower end of its full-year guidance from $755 million to $760 million. At the higher end, the company expects to hit revenue of $775 million in the current year. The midpoint of its current guidance range would translate to an 11% increase in revenue this year.

Of that, AI is expected to contribute 3 percentage points to DigitalOcean’s growth this year. However, don’t be surprised to see AI becoming a bigger contributor to the company’s growth in the future thanks to the market it is targeting. On the company’s latest earnings conference call, CEO Paddy Srinivasan remarked: “We’re seeing strong revenue growth for our early stage AI solutions as we continue to ramp up our initial GPU capacity through the first part of this year. And our expectations are that demand will continue to outstrip supply for the foreseeable future.”

DigitalOcean is targeting customers who are looking to deploy a variety of smaller AI models instead of using just one large language model (LLM), which can be costly to train and deploy. The demand for this service is strong — DocuSign’s annual recurring revenue from its AI platform-as-a-service (Paas) offering increased an impressive 128% quarter over quarter in Q1.

Demand for DigitalOcean’s AI GPU-as-a-service is also increasing at a nice pace. The company launched this service in January this year and witnessed a 67% jump in consumption from March to April. Both markets present a huge growth opportunity for DigitalOcean.

According to third-party estimates, the AI PaaS market is forecasted to clock annual growth of almost 21% through 2028, generating almost $15 billion in revenue at the end of the forecast period. Meanwhile, the global GPU-as-a-service market could clock annual growth of almost 36% through 2032 and generate close to $50 billion in annual revenue.

DigitalOcean could therefore drive greater spending from its customer base in the long run, leading to higher average revenue per user (ARPU). The company’s ARPU increased 8% year over year in Q1 to $95.13, while its overall customer base increased 3%. While these numbers don’t seem very attractive right now, the increasing adoption of its AI services could help accelerate its growth, which is why analysts are expecting it to grow at a faster pace.

Stronger growth and an attractive valuation make it buy-worthy

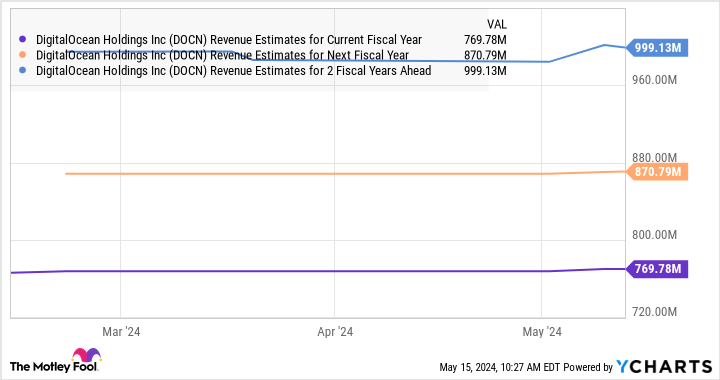

We have already seen that Digital Ocean is expected to deliver 11% revenue growth in 2024. However, as the following chart indicates, the company’s top-line growth is set to improve from 2025.

What’s more, investors can buy this AI stock at just 5.3 times sales right now. That’s lower than the U.S. technology sector’s sales multiple of 7.2. Assuming DigitalOcean is rewarded with a higher sales multiple after three years thanks to its AI-fueled growth, and that it trades at the tech sector’s average and hits almost $999 million in revenue in 2026 per the chart above, its market cap could increase to $7.2 billion.

That would be double DigitalOcean’s current market cap. Investors would do well to buy this potential AI winner while it is still cheap.

Should you invest $1,000 in DigitalOcean right now?

Before you buy stock in DigitalOcean, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and DigitalOcean wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $566,624!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, DigitalOcean, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Here’s My Top Artificial Intelligence (AI) Stock to Buy and Hold was originally published by The Motley Fool