Is ASML’s Big Sell-off a Warning Sign to Artificial Intelligence (AI) Investors?

Investors?")

ASML is a key supplier for all chip manufacturers.

ASML (ASML 2.04%) probably ranks among the most essential companies in the world today, yet few people know what they do. Part of this stems from being headquartered in the Netherlands rather than the U.S., but that doesn’t excuse investors from not knowing about it, especially since its market cap places it among the top 30 largest companies in the world.

ASML recently had a sizable sell-off and fell 10%. Given how vital ASML is to essentially all electronic devices, should artificial intelligence (AI) investors heed this warning signal?

ASML’s machines are vital for AI chips

ASML is a vital company in the microchip supply chain. It is the only company in the world that has its technology, so any company wanting to make cutting-edge chips must work with ASML.

Image source: ASML.

Currently, ASML’s extreme ultraviolet machines allow its users to fabricate as thinly as 3 nanometers (nm). For reference, DNA is about 2.5 nm in diameter, and a sheet of paper is anywhere from 80,000 to 100,000 nm thick. However, ASML and its clients are still pushing the limits, as 2 nm chips are expected to debut sometime next year.

Given how integral ASML is to the chip supply chain, many investors assume that it should be doing great, as AI chips are in great demand right now. However, ASML isn’t seeing that demand. In its first-quarter results, ASML had sales of 5.29 billion euros, down from last year’s 6.75 billion euro mark.

However, this was completely expected, as management is forecasting that 2024’s sales would roughly equal 2023’s.

This may confuse some investors with the high demand for AI chips. However, one thing to remember about the chip market is that it’s cyclical. These machines take a long time to build and are purchased years before being installed and used in a full-production setting. So, using ASML as a bellwether stock for the entire chip industry isn’t a great idea, as it only indicates chip demand years in advance.

Still, if you have a long-term investing mindset, this short-term sell-off may give investors the entry point they need.

ASML’s stock is still pricey for its long-term projections

Prior to reporting its Q1 results in ASML’s investor presentation, it stressed some of its long-term projections. In 2025, it expects revenue between 30 and 40 billion euros. Compared to 2023’s 27.6 billion euro mark, this would be strong growth for the business. Additionally, in 2030, it expects between 44 and 60 billion euros in revenue, with a higher gross margin to boot.

Should ASML hit the midpoint of the 2030 projections (52 billion euros with a 58% gross margin), investors could probably expect profit margins in the mid-30% range, as ASML’s current profit margins with around 50% gross margins are in the high 20% range.

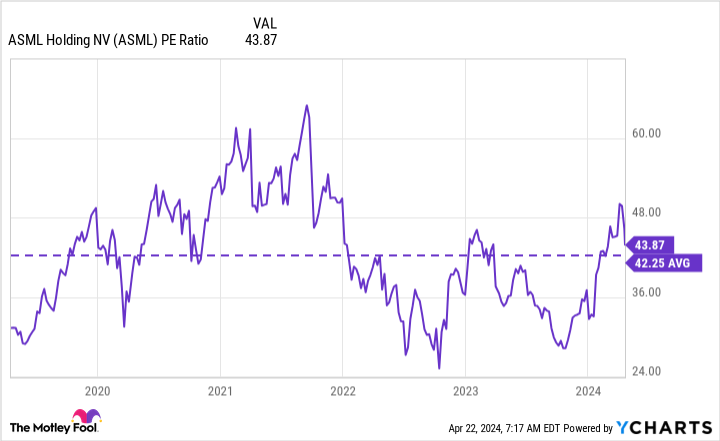

If it delivers 35% profit margins, that will give ASML a hypothetical 2030 net income of 18.2 billion euros. Over the past five years, ASML has traded for around 42 times earnings — a very expensive mark. Taking a more conservative valuation approach (35 times earnings) gives us a margin of safety in the model to have a little bit of error in other areas.

ASML PE Ratio data by YCharts

Should ASML achieve its earnings projections and be valued at 35 times earnings, the company would be worth around 637 billion euros, or $601 billion. At its current valuation of $354 billion, this would indicate a 70% upside, which seems great. However, if you calculate the compound annual growth rate (CAGR) of that figure, it comes out to under 8% per year.

With the long-term average CAGR of the S&P 500 around 10%, ASML’s current growth projections could result in a loss to the market if investors bought now.

So, while ASML’s weak year may have caused a sell-off, it hasn’t sold off enough to warrant buying. Still, ASML’s results shouldn’t be used as an indication of the broader AI industry, as many businesses are still doing incredibly well.