Is This Top Cybersecurity Stock Now Dead Money?

Fortinet appears to be going through growing pains, but that may be the wrong way to look at the situation.

Shares of Fortinet (FTNT 0.09%) once again gave back recent gains as investors digested another muted outlook from the cybersecurity company’s management team. After several years of accelerated growth due to pandemic lockdowns and organizations upgrading their IT infrastructure as a result, Fortinet’s historically hardware-based business is going through a cyclical downturn.

Ultimately, this has led to lackluster stock performance for going on three years now. Does this mean Fortinet stock is now dead money? Or is there more to the story?

A good quarter, but investors are worried

Fortinet actually had a decent first quarter of 2024. Revenue came in at $1.35 billion, up a modest 7% year over year and near the high end of guidance management provided three months prior. Generally accepted accounting principles (GAAP) earnings per share (EPS) were up 26% year over year to $0.39. On an adjusted basis, EPS was also up 26% from last year to $0.43, topping the high end of adjusted EPS guidance of $0.39.

The company even raised its full-year 2024 outlook. It now expects revenue to be in the range of $5.745 billion to $5.845 billion (previously guided to $5.715 billion to $5.815 billion three months ago), implying growth over 2023 of just over 9% at the midpoint. Adjusted EPS guidance was also raised to a range of $1.73 to $1.79 (previously $1.65 to $1.70), implying growth of 8% at the midpoint.

Free cash flow (FCF) fell a bit to $609 million versus $647 million a year ago. Interestingly, no buybacks were made this quarter. Is Fortinet gearing up for a big move? Or just retooling for new product launches? Either way, there was a big jump in liquidity on balance, with cash and short-term investments now up to $3 billion, offset by long-term debt of just $993 million.

So far so good, so why the market’s angst? As mentioned last quarter (and the last few quarters before that), Fortinet’s billings have investors fretting. Billings are invoiced amounts customers owe. For a tech company, especially one like Fortinet that is in a multiyear pivot to more software business, billings can be an important indicator of future growth.

For full-year 2024, billings expectations were left unchanged at $6.4 billion to $6.6 billion. Billings were $6.4 billion in 2023, so it appears Fortinet’s long-term trajectory is seriously losing steam.

Retooling to address new cybersecurity needs

As mentioned at the outset, Fortinet is historically a hardware-based network security provider. Its expansion has been tied to the sale of firewall network security devices, and like any hardware sale, growth can come and go in waves. After a massive growth cycle during the pandemic, Fortinet’s hardware sales are now in a down cycle. Product sales fell 18% year over year in Q1 to $409 million.

But these days, Fortinet’s recurring services business (driven by a growing portfolio of software) is rising fast. That segment was up 24% year over year to $944 million. Most of this software expansion has been completely internal development of services, versus Palo Alto Networks‘ (PANW 0.61%) heavy acquisition strategy in recent years.

This unified OS alone doesn’t solve some problems like customer data and operations silos, where parts of the business can remain unprotected. This is increasingly the case as organizations are adopting a “hybrid cloud” strategy where parts of their business remain in more traditional IT (on-prem, like computers and servers in an office) and other parts are migrated to the cloud (either a private or public data center, accessed via a network connection or the internet).

Solving this pain point is where newer products like secure access service edge (SASE) come in. Palo Alto Networks is recognized as the leader in SASE, and newer cloud-based companies like Zscaler (ZS 1.55%) have been building all cloud-based alternatives called SSE (secure service edge, a subset of a complete SASE solution). However, co-founder and CEO Ken Xie explained on the Q1 earnings call that Fortinet could have a long-term advantage over the competition, including the same OS for its new service as its older ones, flexibility for how customers deploy the SASE security service (it could be in the cloud, or on-premises), and ability to cover multiple computing endpoints with a single software deployment.

Put simply, billings are down for a variety of reasons, all of them related to Fortinet building this new SASE and other cybersecurity services. A bit of growth is being sacrificed this year as a result, but Xie and the top team still anticipate a reacceleration of expansion in the second half of 2024.

Fortinet could be cooking up great things

There’s no denying that Fortinet isn’t a “cheap” stock. Shares currently trade for 38 times trailing-12-month GAAP EPS, or 27 times trailing-12-month free cash flow. This premium price is why the stock has been so volatile over the last few years.

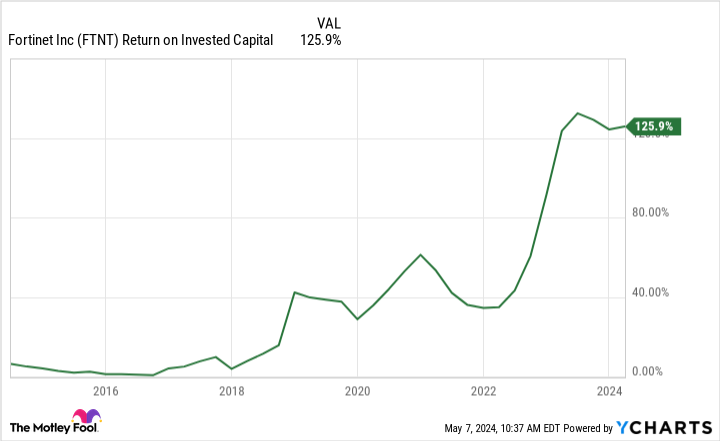

However, true value is found not in past financial metrics, but in future expectations. If Fortinet comes out of this current down cycle and delivers great returns on its current investments (like the new SASE service) as it has in the past, this could actually be a solid long-term bet.

Data by YCharts.

I already have a full position in the stock, as Fortinet has been a core cybersecurity holding in my portfolio (along with Palo Alto Networks) for years. Thus, I’m not buying more at this time. But I’m also more than happy to hold and wait for a resumption of growth given the track record.