More neobanks are becoming mobile networks — and Nubank wants a piece of the action

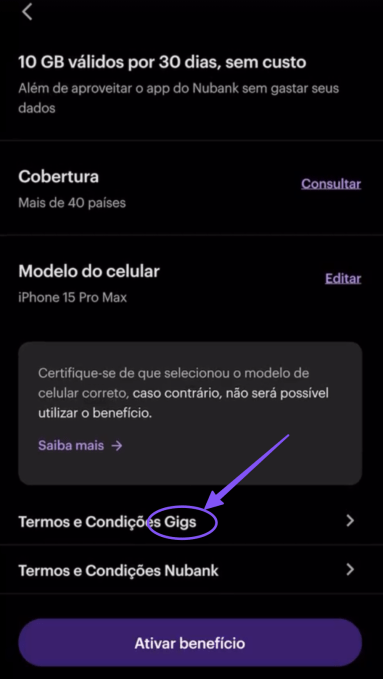

Nubank is taking its first tentative steps into the mobile network realm, as the NYSE-traded Brazilian neobank rolls out an eSIM (embedded SIM) service for travelers. The service will give customers access to 10GB of free roaming internet in more than 40 countries without having to switch out their own existing physical SIM card or eSIM.

The launch comes shortly after news first emerged that Brazil’s National Telecommunications Agency (ANATEL) had quietly greenlit plans for Nubank to become a mobile virtual network operator (MVNO) in partnership with wireless giant Claro. While that plan remains in the early stages and Nubank hasn’t confirmed any of the launch details (the company also declined to comment for this article), we can now confirm that it’s at least tiptoeing into the mobile network sphere — a growing trend within the fintech fraternity.

From neobanks to neo-MVNOs

Neobanks — a new breed of financial institution that serve as digital-native challengers to established banking incumbents — follow in the footsteps of traditional banks by offering ancillary services to target new customers, such as budgeting tools, data and spending insights, and easy access to the stock market. While neobanks have surged in popularity, so has the MVNO (mobile virtual network operator) market, driven by the rise of eSIM, the cloud and the proliferation of third-party software that makes all-digital distribution strategies a cinch.

Nubank sits at the intersection of these trends.

The 10-year-old Brazilian company has been on a tear of late, its valuation surging by around 170% in the past year and hitting an all-time high of $58 billion in March. The company swung from a $9 million net loss in 2022 to a $1 billion net profit last year, a trend that’s continuing into 2024 with record revenues in Q1 and its net profit more than doubling on the previous year’s corresponding period. Nubank also passed 100 million customers across its core markets of Brazil, Mexico and Colombia, where it operates a range of services including bank accounts, credit cards, loans, insurance, investments and — now — a mobile data service for travelers.

The new service is aimed at customers of Nubank Ultravioleta, a premium subscription it launched three years ago with bundled benefits such as insurance, higher credit limits, cashback, family accounts and more.

Last month, Nubank revealed it was entering the travel sector with the impending launch of a new “global account,” partnering with European fintech Wise to offer Ultravioleta subscribers low-fee international money transfers. As part of this, the company is now launching an eSIM service for those with compatible smartphones, with 10GB of data for travelers in the U.S., Latin America and Europe. The eSIM is activated through the Nubank app, with the underlying infrastructure powered by Gigs, a platform that gives budding mobile network providers everything they need through a single API — basically what Stripe has been doing in finance, but for mobile phone plans.

Gigs is backed by the likes of Google’s early-stage venture capital arm Gradient Ventures and Uber CEO Dara Khosrowshahi.

“Bundling mobile plans represents a powerful lever for neobanks to turn irregular users into monthly paying subscribers, encourage upgrades to premium features, and create an ecosystem where banking acts as a hub for multiple value-added services,” Gigs co-founder and CEO Hermann Frank told TechCrunch.

Nubank’s launch echoes moves elsewhere in the fintech fray. In February, Revolut — a $25 billion U.K. neobank — launched a similar eSIM service for premium subscribers. And last year, Indian neobank Zolve also added mobile networks to its arsenal of services so immigrants can not only have their banking set up before arriving in the U.S., but have a mobile service ready to go on arrival too.

This highlights the synergies between financial services and mobile communications — both are essential for people to function today, but both traditionally have similar hurdles, particularly for those arriving in a country for the first time. We’ve seen carriers launching banking services as T-Mobile has done in the U.S. with T-Mobile Money, while traditional banks have gone in the other direction too, evidenced by Brazil’s Banco Inter and Standard Bank in South Africa, both of which have launched their own MVNO services.

“Our bank interaction today is already focused on our mobile number, either for banking itself or for security checks,” Allan T. Rasmussen, a telecoms industry consultant, analyst and MVNO specialist explained to TechCrunch. “Mobile operators are moving in on the banking business, trying to become banks themselves, and traditional banks and fintechs are doing the same by becoming MVNOs.”

But neobanks, in particular, are synergistic with MVNOs: They are both “virtual,” with technology playing a big part in their respective offerings, often only with online support and account access. They are also both marketed as having lower overheads, which gives them greater agility and the ability to offer lower prices versus the incumbents. And as we’ve seen with Revolut and now Nubank, eSIM is driving this cross-pollination further, as they jostle for mindshare, revenue and access to customer data and touch points.

“To be successful as an MVNO, you need a distribution channel — that’s the first test of your pitch to an operator,” James Gray, managing director at telecom industry consultancy Graystone Strategy, told TechCrunch. “Banks already have this with high street banking or through websites and apps. However, the recent move from Revolut — and I suspect other neobanks in the future — is interesting because these are not traditional organizations. Their whole remit is to challenge the status quo and they are doing this very successfully in banking, so why not a banking telecoms fusion? They have the channels and the brand pull.”

MVN… no?

One small catch: The neobanks aren’t actually positioning themselves as MVNOs with their new travel eSIM services. A Revolut spokesperson told TechCrunch in February, “Revolut is not becoming an MVNO but has partnered with 1Global, which brings together many MVNO and roaming access agreements into a single network to create a global footprint of the best carriers.”

MVNOs are independent mobile services built atop carriers’ infrastructure, and there are many different mobile virtual network enablers (MVNEs) and aggregators (MVNAs) out there (like 1Global) that help companies launch mobile networks, taking care of SIM provisioning, billing and the like. Although Revolut doesn’t offer voice and SMS, or allocate a phone number, it still leans on carrier infrastructure via an MVNE to offer an own-brand mobile data service, which sounds a lot like Revolut becoming an MVNO.

But calling itself an MVNO could invite extra regulatory oversight. Although banks are already tightly regulated as financial institutions, being classed as a telecommunications company would likely usher in further regulatory obligations. This is something we’re seeing play out right now in the U.S., with the Federal Communications Commission (FCC) trying to determine whether connected cars should be classed as MVNOs, following a New York Times report into how connected cars are being used by abusive partners to track their victims.

While Nubank is indeed preparing to launch an MVNO service in its domestic Brazil, its travel eSIM service is more straightforward to bring to market due to its partnership with Gigs, as that partner assumes all the regulatory compliance complexities that come with the territory.

“Telecom is a highly regulated industry across all countries, and a key part of Gigs’ end-to-end value proposition is that we abstract away all regulatory complexity for our customers,” Frank said. “To do so, Gigs almost always acts as the licensed carrier of record, which means the burden of compliance falls on Gigs and not with our customers. This allows our customers to launch their own mobile service, without legally becoming a provider in a regulated industry.”