Rubrik: Latest Cybersecurity IPO – Initiating Coverage, Buy Rating (NYSE:RBRK)

")

hapabapa

Rubrik (NYSE:RBRK) is the first major software IPO of the year and came public to great success, with the stock trading 15% higher at the close. I analyze the financial results and discuss the confusing difference between revenue and ARR growth. The company is not yet profitable, but I expect solid margins over the long term. Following the IPO, the company should have ample net cash on the balance sheet, though I note that operational cash burn is already quite modest. It’s unclear exactly how much top-line growth might decelerate moving forward, but current valuations look buyable nonetheless. I’m initiating coverage with a buy rating.

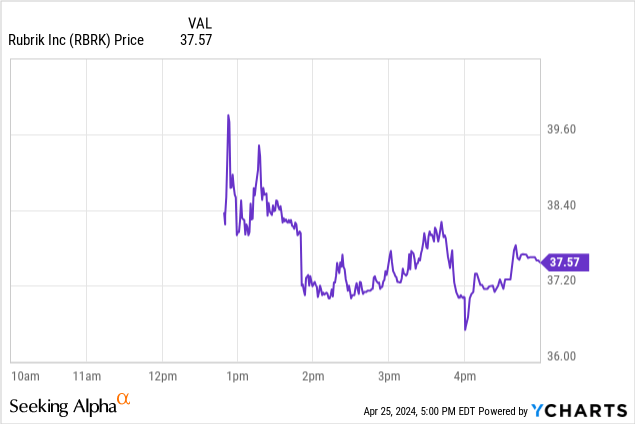

RBRK Stock Price

RBRK priced its IPO at $32 per share, above its initial $28 to $31 range. The company sold 23.5 million shares and raised $752 million. The stock closed its first day of trading at $37.00 per share, representing a 15.6% first day jump.

RBRK Stock Key Metrics

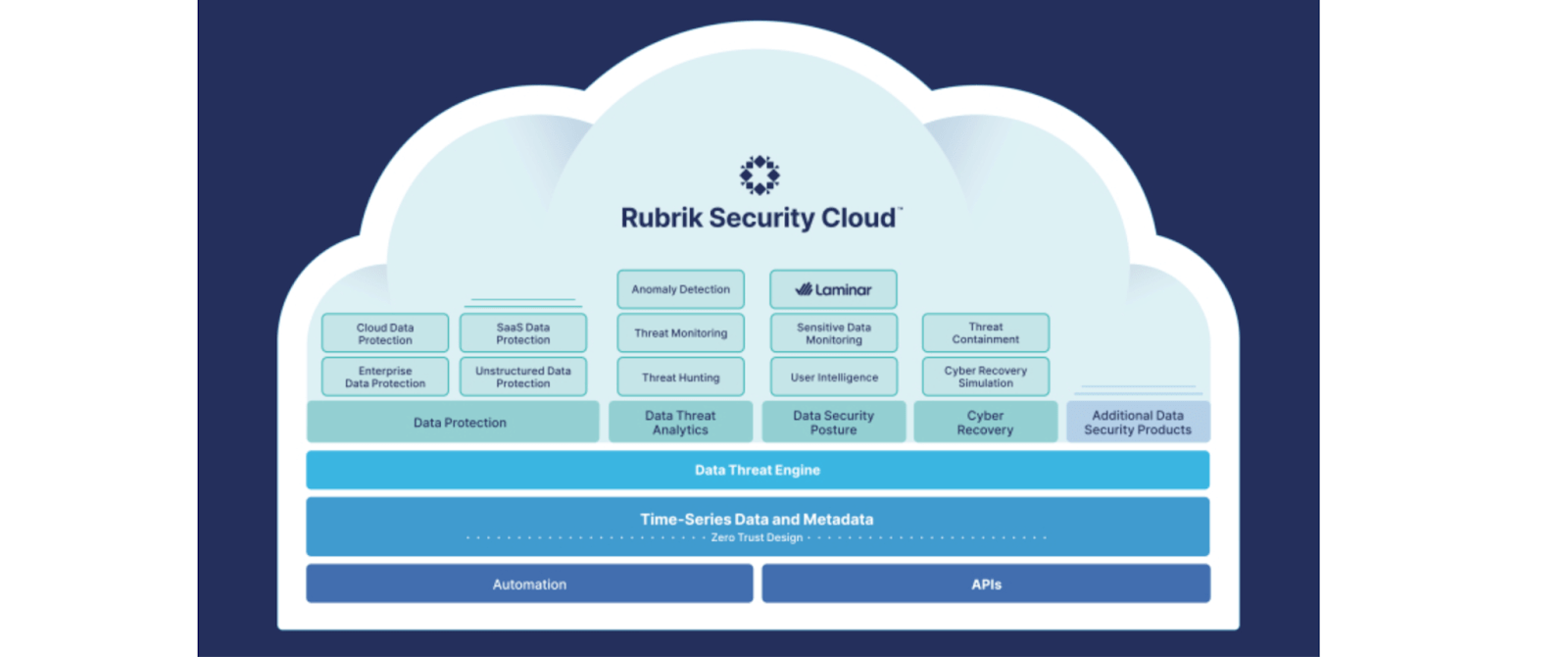

RBRK is a cloud data management and data security company. As stated in the S-1, “organizations around the world rely on Rubrik to achieve business resilience in the face of cyberattacks, malicious insiders, and operational disruptions.”

Rubrik S-1

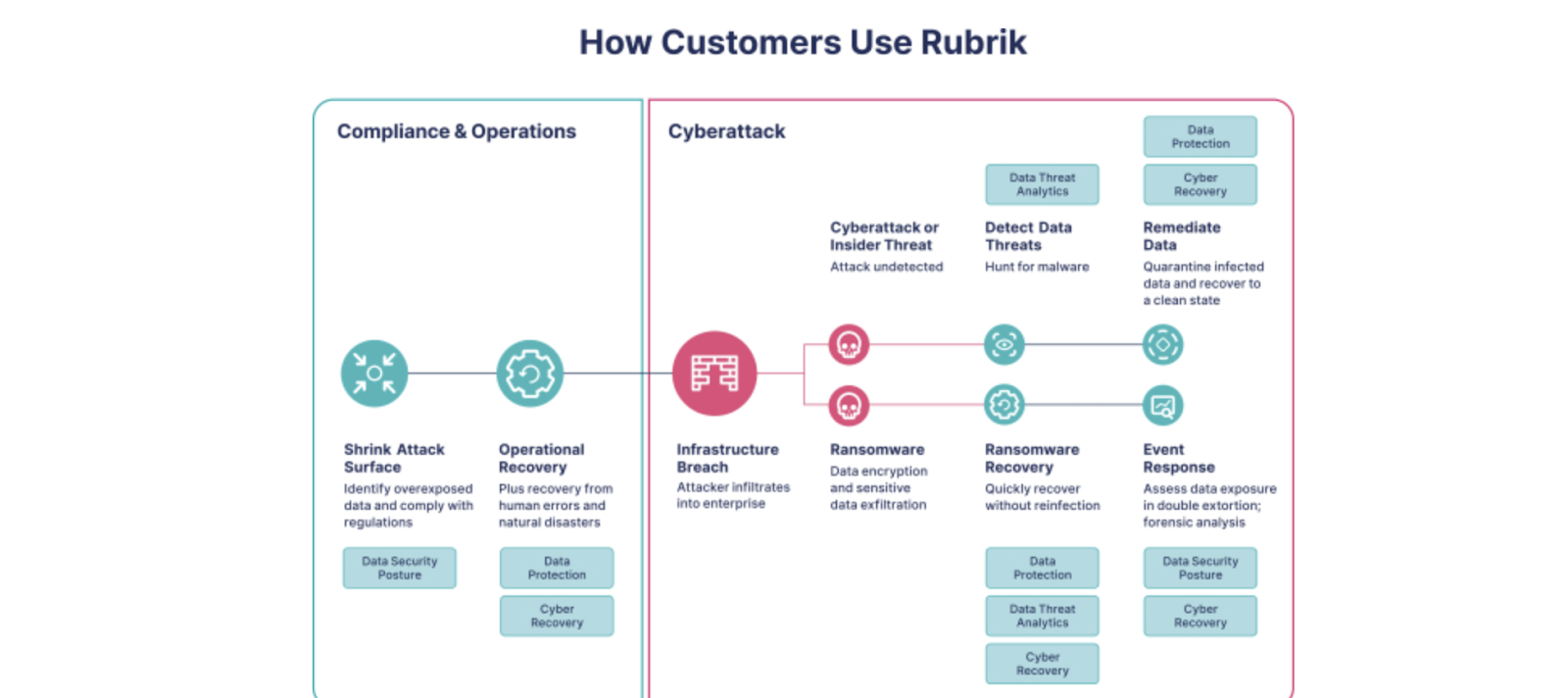

An easy way to understand what RBRK does is that it helps its customers back up their data, which is crucially valuable especially in the event of a cyberattack, when customers would rely on these backups to ensure no disruption to their business. I suggest watching Rubrik’s video for a more detailed explanation of their business.

Rubrik S-1

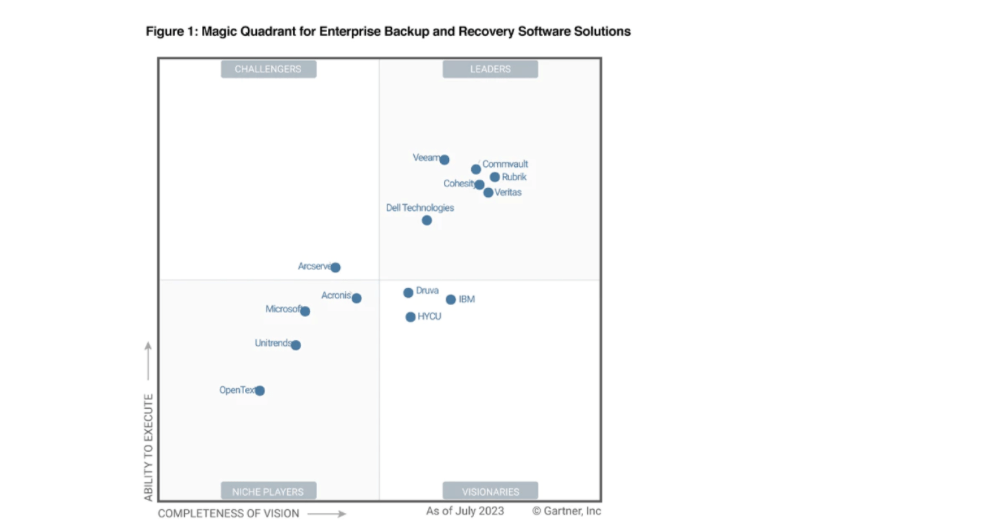

RBRK operates in a highly competitive space but is rated by Gartner as being one of the market leaders. I note that Commvault (CVLT) is a noteworthy competitor and is also publicly traded.

Rubrik

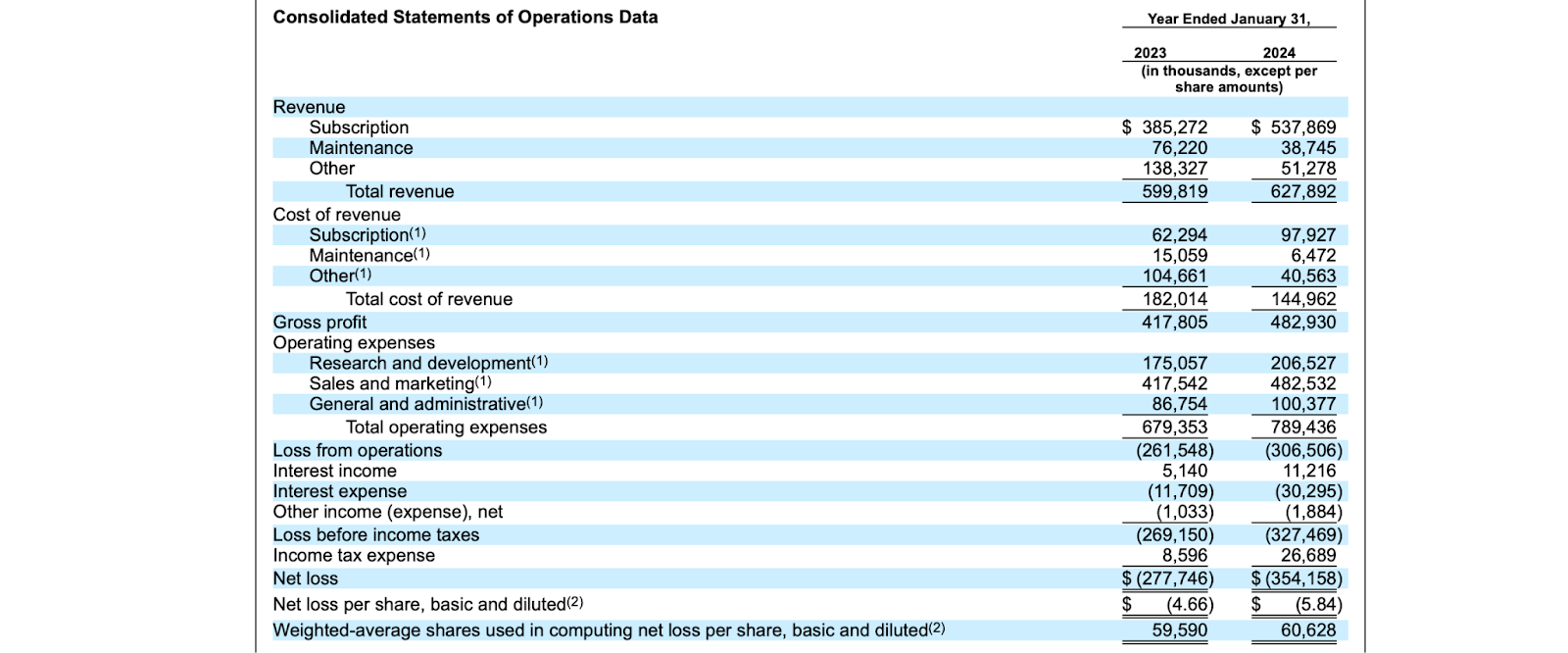

In this past year, RBRK saw revenues grow by only 4.7% YoY to $627.9 million. The company remains far from GAAP profitability though I note that the free cash flow burn was only $24.5 million for the full year.

Rubrik S-1

The company has been transitioning customers from perpetual licenses to subscription-based offerings over the last two years. The company discloses subscription annual recurring revenue (‘ARR’) as being a more important metric to track. Subscription ARR jumped 47% YoY to $784 million as of the end of the year. Management noted that “approximately four percentage points are a result of transitioning our existing maintenance customers to our subscription editions.” This is an important detail because subscription ARR growth holds little meaning if much of it is just coming from converting existing customers (which is not the case here). The company posted an impressive 133% subscription dollar-based net retention rate, which would be one of the strongest, if not the strongest in the tech sector.

Rubrik S-1

That said, I note that the dollar-based net retention rate has decelerated rapidly over the last few quarters, and I expect further deceleration moving forward.

Rubrik S-1

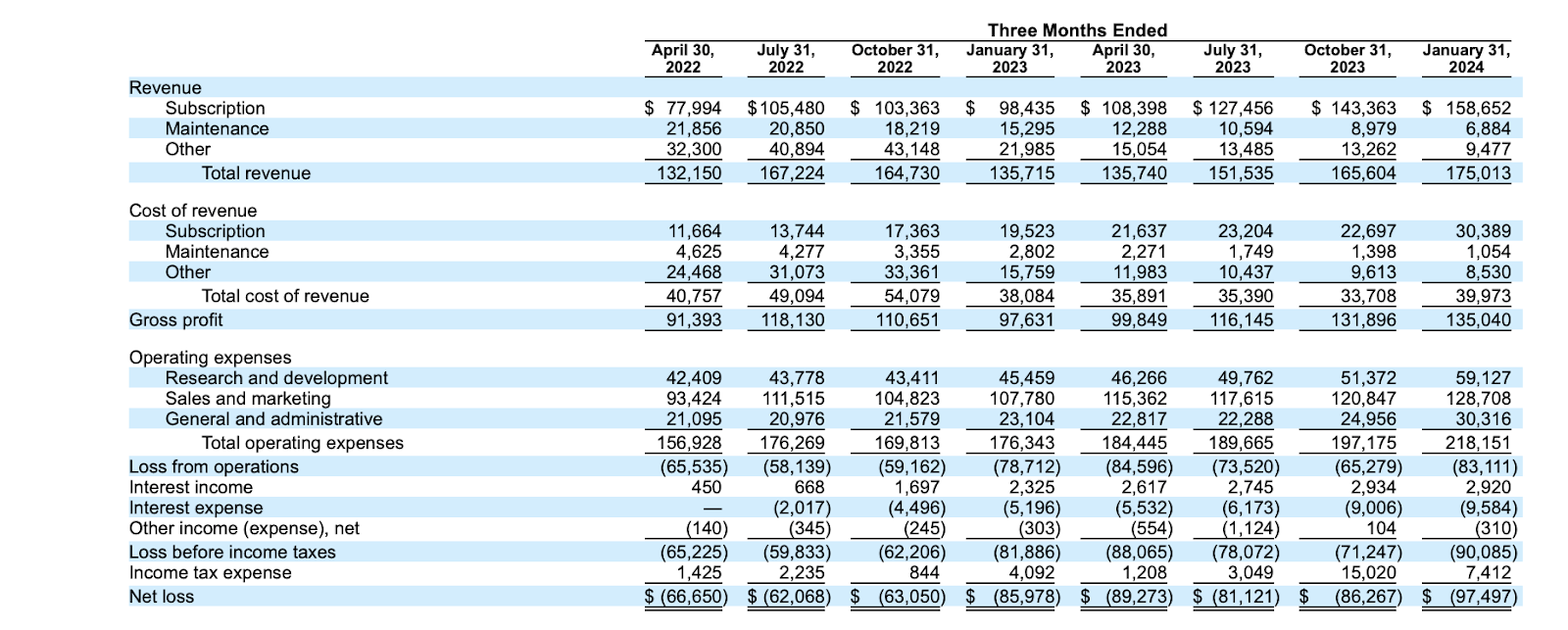

We can see a quarterly snapshot of the financials below. As we can see, the company has not been so aggressive in cost discipline as tech peers – I’m curious to see if management changes its tune now that they’re a public company.

Rubrik S-1

With subscription gross margins hovering above 80%, operating leverage is key to drive sustainable profitability. RBRK ended the year with $279 million of cash vs. $293.6 million of debt, but did raise another $752 million of cash in the IPO, giving it just over $1 billion of cash and $800 million of net cash.

Is RBRK Stock A Buy, Sell, or Hold?

Let’s now calculate the current valuation and a fair value target for the stock. I count just over 60 million shares outstanding.

Rubrik S-1

Together with the 74.2 million shares from the conversion of preferred stock as well as additional RSUs and outstanding options, we arrive at 188 million shares outstanding.

Rubrik S-1

Throw in the 23.5 million shares issued in the IPO, and we arrive at around 211 million shares outstanding. It’s always difficult to accurately pinpoint shares outstanding, and I note that my calculated number is a bit higher than that reported elsewhere.

The company currently trades at a market cap of around $7.8 billion and an enterprise value of $7 billion. It’s difficult to value the stock on revenues due to the ongoing transition to subscription offerings. Assuming 25% ARR growth this year, the stock trades at 8x sales and 7x EV/S. It remains to be seen if RBRK will be valued more like a typical data storage company like Box (BOX), which trades at 3.7x sales, or like a cybersecurity stock like Crowdstrike (CRWD), which trades at 18x sales. My guess is that it will be valued more like a cybersecurity stock, but I’m doubtful that it will command such rich multiples due to its business not appearing to have as much cross-selling opportunities. I do not mean to suggest a lack of future growth – RBRK appears to offer exposure to growing amounts of data – but I caution investors from thinking that this should double quickly, as there are noted differences between typical platform cybersecurity names. I can see subscription ARR growth hovering around the 20% to 25% range over the next two to three years. That might justify a valuation of around 9x sales. Based on 25% long-term net margins, that would equate to a valuation of around 36x long-term earnings, which seems appropriate relative to that top-line growth rate. That equates to a stock price of around $44 per share, after giving some credit to the net cash on the balance sheet.

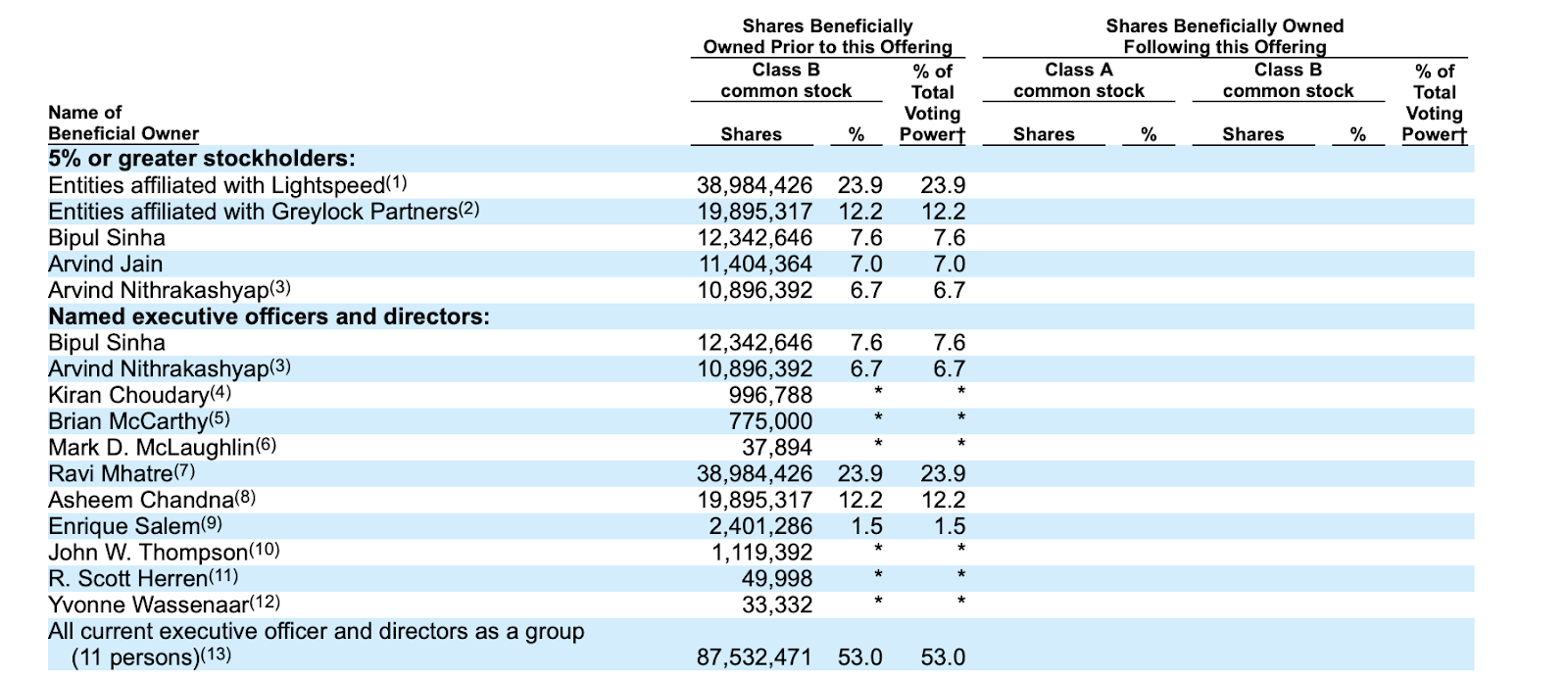

I note that insiders own a great deal of stock in the company, including 87 million shares owned by the executive officers and board of directors.

Rubrik S-1

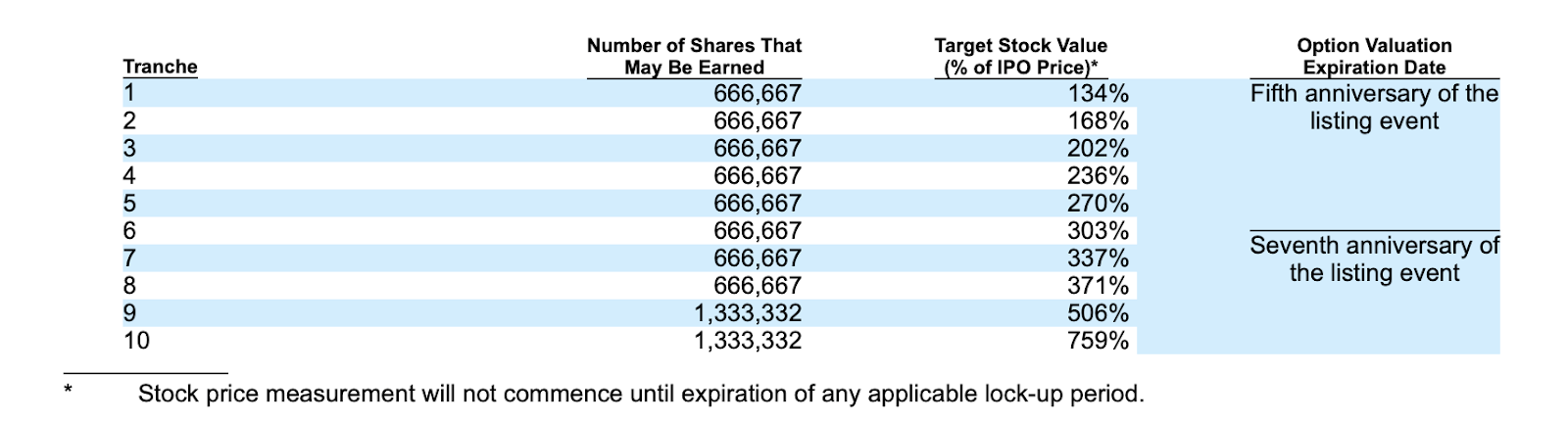

I should also note that CEO Bipul Sinha has an equity performance plan in which he receives a generous amount of stock assuming that the stock delivers strong returns over the coming years.

Rubrik S-1

However, I caution against getting too excited about the above performance plan given that many tech stocks had similar programs heading into the 2022 tech stock crash, which ultimately proved meaningless.

Rubrik Stock Risks

RBRK operates in a very competitive space. From my perspective, it’s not clear if RBRK has a clear advantage over competitors like CVLT, if at all. I note that CVLT is seeing ARR growth in the 15% range, and it’s possible that RBRK might see its own growth rates decelerate far more rapidly than expected. With the company not yet profitable, there’s no explicit downside support to the valuation, and I can see the stock undergoing great volatility if investors were to lose faith in the long-term growth trajectory of the business.

Conclusion

RBRK is an interesting new IPO, offering yet another way to invest in secular growth themes like data and cybersecurity. The company has a strong balance sheet, and I would not be surprised to see a greater focus on driving profitability moving forward. It’s unclear where subscription ARR growth lands over the coming quarters, but the current valuation is not pricing in lofty numbers. I’m initiating coverage with a buy rating and $44 price target.