Salesforce Overreaction – CRM Stock Looks Deeply Undervalued Based on Its Massive FCF

Salesforce (CRM) stock has dropped almost 20% in the past two days from $271.62 to $218.07. The market overreacted to a slight miss in Salesforce’s quarterly revenue reported on May 29. This is even though Salesforce generated a massive 66.3% free cash flow margin, guiding for 31.8% for the year. As a result, CRM stock looks deeply undervalued here.

I discussed the Salesforce guidance in my May 27 Barchart article, “Salesforce Earnings Out This Week – CRM Stock Looks Undervalued Based on Its Free Cash Flow.” The company has kept its operating cash flow (and by implication the free cash flow) guidance intact.

Massive FCF Margins

Salesforce said its operating cash flow for this fiscal year will remain at a growth rate of 21% to 24% Y/Y. Last year it made $10.23 billion in operating cash flow. So this implies that it could make up to $12.685 billion this year.

After a small capex spend, that implies FCF could be about $12.1 billion this year.

The company also said that its revenue will range between $37.3 billion and $38 billion this year. That implies its FCF margin this year will be at least 31.8% to 32.4%, or about 32% on average.

Keep in mind that this quarter it generated $6.084 billion in FCF or half the projected $12.1 billion expected for the full year. That FCF also represents a massive 66.3% of its $9.167 billion in quarterly sales.

In other words, FCF could likely exceed the expected $12.1 projected for the year. But, just to be conservative, let’s assume that its 32% FCF margin plays out this year. The stock will still be undervalued. Here’s why.

Target Price Based on FCF Yield Metrics

For example, analysts now project between $37.88 billion and $41.47 billion in sales over the next 2 years. That implies the next 12 months (NTM) revenue will be on a run rate of $39.675 billion. After applying a 32% FCF margin, the projected FCF could be $12.7 billion.

As a result, using a 4.75% FCF yield metric, which is the same as multiplying FCF by a low 21x multiple, will result in a projected market cap of $266.7 billion (i.e., $12.7b x 21). That is $56.7 billion higher than its present $210 billion market, or 27% higher.

Just to be even more conservative, let’s use a 20x multiple or an FCF yield of 5.0%. That results in a potential $254 billion market cap, or 21% higher than today’s market cap.

That implies that CRM stock is worth between 21% and 27% more, or between $263.86 and $276.95 per share. On average the price target is at least $270.41.

One way to play this is to sell short out-of-the-money (OTM) put options. That way the investor can make extra income while waiting for the stock to fall before buying.

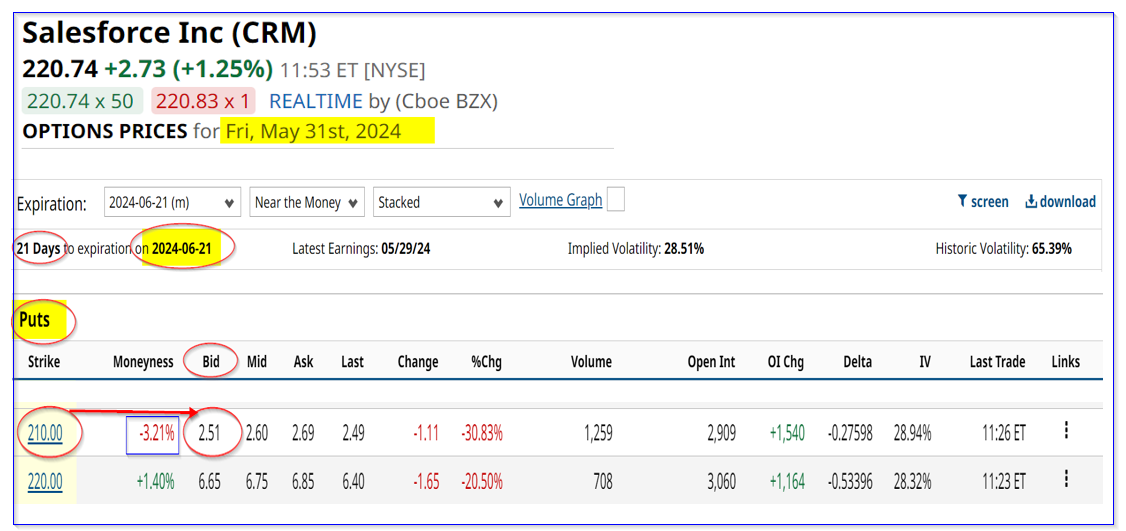

Shorting OTM Puts in CRM Stock

For example, look at the $210 put option expiring in three weeks on June 21. It is trading for a price of $2.51 on the bid side at a strike price that is over 3% below today’s price. That represents an immediate yield of 1.20% (i.e., $2.51/$210.00).

This shows that there is good income that can be made shorting OTM puts. Moreover, if CRM falls to $210 on or before June 21, the investor will be forced to buy 100 shares per contract at that price. But I have shown that this is a good entry point, especially since CRM stock is so undervalued now.

This play works well for existing shareholders who want to make extra income, and would not mind buying more shares at a lower price if forced to. That way they can also get any upside in CRM stock while also making extra income.

The bottom line is that CRM looks cheap here and shorting OTM puts in nearby expiration periods is a good way to play this.

More Stock Market News from Barchart

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.