Salesforce Stock Sinks on Weak Outlook. Time to Buy the Dip?

Shares of Salesforce (NYSE: CRM) were selling off after the customer-relationship management (CRM) software company issued weaker-than-expected second-quarter guidance.

Let’s take a closer look at the company’s recent earnings report, why the stock is selling off after maintaining its full-year forecast, and whether or not the sell-off creates a good buying opportunity.

RPOs and Q2 guidance in focus

Salesforce saw its first-quarter revenue rise 11% year over year to $9.13 billion, which was at the lower end of its prior guidance. Subscription and support revenue jumped 12%, or 13% in constant currencies, to $8.59 billion.

Current remaining-performance obligations (cRPOs) increased 10% year over year to $26.4 billion. cRPO is a metric used by software-as-a-service (SaaS) companies to give investors an indication of future revenue that will come from existing contracts over the next 12 months. The latest figure was a deceleration from the 12% to 14% cRPO growth it generally saw last year.

Looking ahead, Salesforce forecast Q2 revenue to come in between $9.2 billion to $9.25 billion, representing 7% to 8% year-over-year growth, with adjusted earnings per share (EPS) of $2.36. That was below analyst expectations of $9.37 billion in revenue and $2.40 in EPS. Stocks are quite often valued based on future expectations, so when a company gives guidance that is below these expectations, it can often cause a stock to fall.

However, Salesforce did maintain its full-year forecast. It is looking for full-year revenue to fall between $37.7 billion to $38 billion, representing 8% to 9% growth, with adjusted EPS of between $9.86 to $9.94. It expects subscription and support revenue to increase around 10% year over year in constant currencies.

The company said it was seeing elongated deal cycles, deal compression, and higher levels of budget scrutiny. Management also noted that the implementation of a new go-to-market strategy could have affected billings.

However, management did say it was seeing momentum with artificial intelligence (AI), especially with its Einstein AI virtual assistant, which can help businesses more effectively and quickly answer customer questions. It also has seen solid results from Slack and its new AI tools, while Tableau and MuleSoft have also been performing well.

Image source: Getty Images.

Time to buy the dip?

Overall, the quarterly results from Salesforce were not that bad, and management did maintain its full-year guidance. Nonetheless, the stock was punished. One of the big reasons for this is that, because of the weak Q2 outlook, there is some fear that another shoe will drop, and the company will have to lower its full-year guidance in the future.

One of the first questions from analysts on its conference call was why didn’t management lower its full-year guidance so the company could get back to beat-and-raise quarters. Exceeding expectations is what often drives stocks in the near term, so the thought of the company just meeting future estimates is not looked upon favorably. Investors rarely get excited when a company meets its forecasts, although investors will drive up the price of a stock when it turns around and beats previously lowered expectations.

Over the long term, though, a near-term expectations game doesn’t matter as much as the company’s performance will matter. On that front, Salesforce remains the leader in CRM, although its growth has slowed.

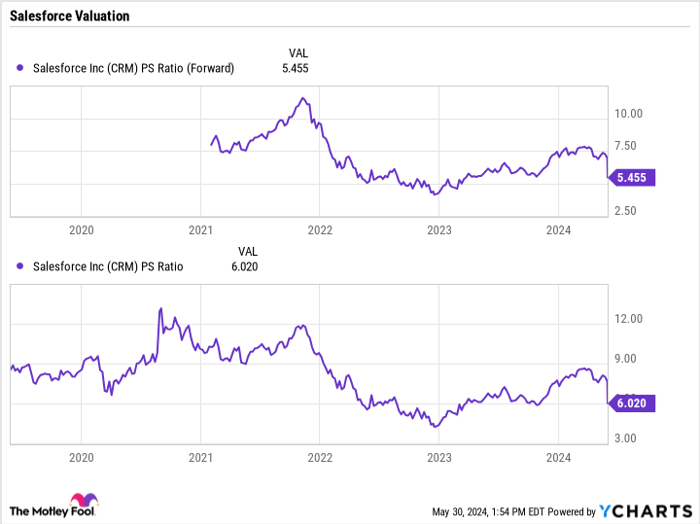

The company currently trades at about 5.5 times price-to-forward sales, which is a relatively inexpensive valuation compared to where the stock has traded previously. However, with slower growth comes a lower multiple.

CRM PS Ratio (Forward) data by YCharts.

The company has about $9.2 billion in net cash and marketable securities, so it could look to continue to make acquisitions to help fuel growth. Recent deals include buying Slack, MuleSoft, and Tableau, all of which have been growing faster than its core business. A strong balance sheet and cash-flow generation give it options.

In the near term, I’d probably stay on the sideline with Salesforce, as I would have preferred the company to have lowered its full-year guidance, especially since the stock got punished for its Q2 forecast anyways. However, I think it still looks like a solid long-term option for investors at current levels as it works to reinvigorate growth through AI.

Should you invest $1,000 in Salesforce right now?

Before you buy stock in Salesforce, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Salesforce wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $671,728!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 28, 2024

Geoffrey Seiler has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Salesforce. The Motley Fool has a disclosure policy.