SoundHound AI’s Business Is Soaring, But Does That Make the Stock a Buy?

SoundHound AI recently posted impressive revenue growth, but there is more than meets the eye with this small artificial intelligence (AI) company.

Artificial intelligence (AI) is making its way into more services by the day. One area that is witnessing some attention at the moment is the intersection between voice and AI.

Smart assistants aren’t really that new, though. Apple integrated Siri into its hardware devices more than a decade ago. Moreover, smart-home devices from Amazon and Alphabet‘s Google have been a favorite among consumer electronics enthusiasts for years.

Nevertheless, perhaps the company that is receiving the most attention in AI-powered voice applications is SoundHound AI (SOUN 1.40%).

Shares of the budding software developer are up 138% so far this year. Moreover, the company just reported impressive earnings for the first quarter of 2024, which ended March 31.

Let’s dive into the financial results and assess if SoundHound represents a lucrative investment opportunity.

Voice and the next frontier of AI

AI-powered voice products are more prolific than you probably think. In addition to Internet of Things (IoT) devices, voice recognition can play an important role in vehicles, fulfilling orders at restaurants, customer service applications, gaming, and more.

According to research compiled by Fortune Business Insight, the addressable market for voice-recognition AI tools is expected to reach $50 billion by 2029, a fourfold increase from its estimated size just two years ago.

Image source: Getty Images.

SoundHound AI’s revenue is soaring…

For the first quarter of 2024, SoundHound AI increased revenue 73% year over year. While this looks impressive on the surface, bear in mind that its sales were only $11.6 million.

Considering management is calling for revenue to be in the range of $65 million to $77 million for all of 2024, it’s clear that the company is still quite small.

Moreover, despite its revenue acceleration, it is burning cash at a higher rate. During the first quarter, the company reported operating losses of $28.5 million. By comparison, SoundHound AI’s operating loss was $25.2 million during the first quarter of 2023.

These losses flowed down to the bottom line, as SoundHound AI’s net income and earnings before interest, taxes, depreciation, and amortization (EBITDA) both fared worse in the latest first quarter compared to the same period last year.

Yet the stock remains pricey and questions linger

There was one part of the earnings report that gave me some hesitation when it comes to buying shares in SoundHound.

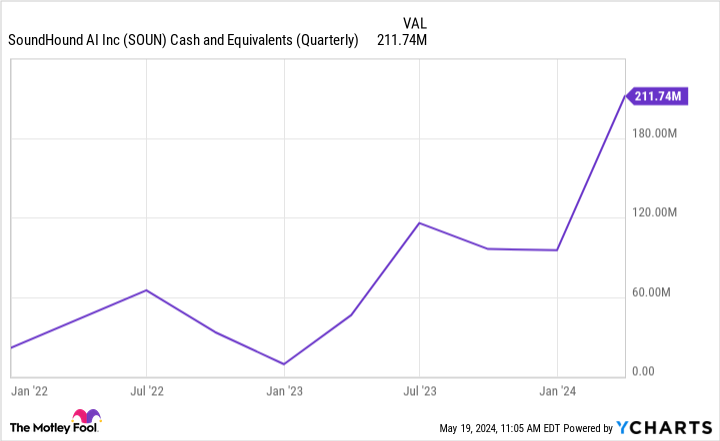

The company ended the quarter with $226 million in cash and equivalents on the balance sheet. This is by far SoundHound’s highest cash balance as a public company. Although this implies strong liquidity, there is more to it than meets the eye.

SOUN cash and equivalents (quarterly); data by YCharts.

Filings show that the company sold $137 million worth of stock during the first quarter. In other words, given the stock price was rising quickly in a relatively short time frame, management decided to sell shares in order to raise capital.

While there is nothing inherently wrong with this approach, keep in mind that when management decided to sell shares, investors were the ones buying into this momentum. Therefore, anyone who purchased shares during the first quarter likely did so at an inflated price.

Moreover, the company won’t be able to resort to stock sales forever. Eventually, it is going to need to prove that it can turn a profit and generate consistent cash flow. If not, investors will eventually sell the stock and the price will plummet.

As of the time of this article, SoundHound AI has a market capitalization of $1.7 billion and trades at a price-to-sales (P/S) ratio of 24.8. By comparison, the P/S of the S&P 500 is 2.5.

Considering SoundHound is nowhere near the size of the companies in the S&P 500, I think its valuation is a bit rich. Furthermore, given the rising number of competitors in the voice-recognition pocket of the AI realm, I’m skeptical of the company’s long-term prospects.

I see this as a company developing interesting technology. But as far as investment prospects are concerned, I think there are too many risks associated with the business.

The stock is overvalued, and buying shares at this level comes with outsize risk. I think an investment in SoundHound AI is speculative, and I see much stronger opportunities in the AI landscape from larger, more established companies.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, and Apple. The Motley Fool has positions in and recommends Alphabet, Amazon, and Apple. The Motley Fool has a disclosure policy.