The Best Is Yet to Come: 1 Fintech Stock to Buy Now and Hold Forever

The fintech landscape is fiercely competitive. But one company is quietly disrupting financial services in a big way.

The financial services industry is hyper competitive. Legacy banks such as Wells Fargo have commanding footprints in the banking realm.

But like any other industry, new players eventually enter the competitive landscape. SoFi Technologies (SOFI -4.06%) is quietly disrupting the banking sector, and you may not even realize it. The company does not have physical branches — it operates solely online.

While this might seem counterintuitive, SoFi’s digital-only model is working. Let’s break down how the company is bringing innovation to the financial services world and assess if now is a good opportunity to scoop up some shares.

SoFi’s business model is unique, and…

It’s not uncommon for people to use a variety of services for their financial needs. For example, a person may obtain a mortgage at Wells Fargo while using Charles Schwab for their brokerage.

SoFi’s goal is to build a one-stop shop for all of your financial ambitions. To achieve this, the company pursued a number of acquisitions to bolster its tech and deepen its product offerings. Today, SoFi allows users to apply for mortgages and student loans, invest in the capital markets, and use the platform for more basic banking services — all in one app.

The subtle benefit of this approach is that SoFi is able to cross-sell a multitude of products and services to its users. In theory, this should help keep people engaged and stay on the platform — thereby providing SoFi with the ability to increase its monetization across the user base.

This strategy is known as a flywheel business model. While this all sounds great on the surface, the proof is in SoFi’s results.

As of Dec. 31, SoFi boasted 7.5 million members on its platform — up 44% year over year. Moreover, each member is using 1.5 products on average.

Let’s explore how SoFi’s growing footprint and penetration of its user base are impacting the financial profile of the business.

Image source: Getty Images.

…the benefits are just beginning to pay off

Since it went public in 2020, one knock against SoFi is that it hasn’t been profitable. But in a way, that makes sense.

In recent years, the company acquired technology platforms Galileo and Technisys as well as mortgage business Wyndham Capital. Acquisitions often come with ongoing integration efforts as well as hefty legal and banking fees.

Moreover, SoFi has also poured significant capital into marketing campaigns as the company seeks to gain critical mass. Since SoFi is a newer option, the company simply does not carry the brand equity compared to legacy financial services providers.

However, during the fourth quarter, SoFi shocked investors when it posted its first ever profit. Furthermore, SoFi Chief Executive Officer Anthony Noto told investors on the fourth-quarter earnings call that the company is in a position to continue driving profitability.

The company’s hefty investments in building out a robust tech platform as well as its aggressive marketing strategy are only beginning to pay off. Although this is encouraging, I see this dynamic as the start of a long-term success story.

SoFi’s valuation is compelling

SoFi is an interesting investment opportunity. On one hand, the company could be viewed as a bank competing with much larger and better-capitalized businesses. But on the other hand, the company’s tech-first approach provides SoFi with a unique competitive advantage, though that’s not reflected in the valuation.

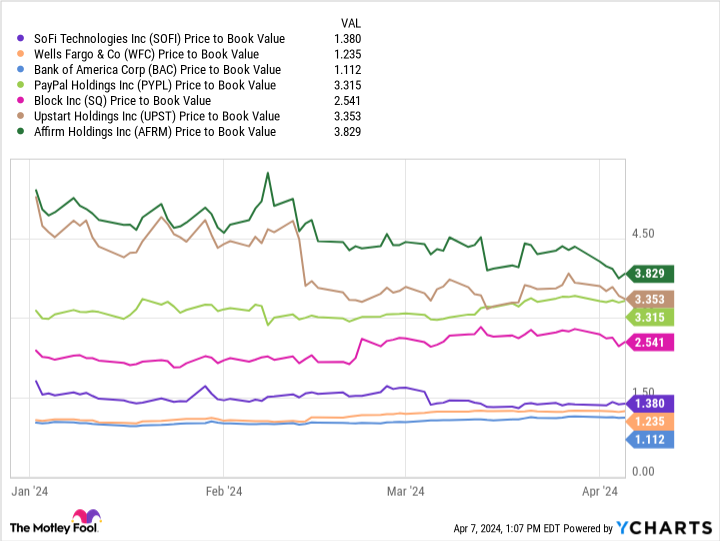

SOFI Price to Book Value data by YCharts

The chart above benchmarks SoFi against a peer set of other companies operating in the financial services industry. With a price-to-book (P/B) ratio of 1.4, SoFi stock is valued at a steep discount to other tech-enabled banking platforms.

Wall Street is taking note of this valuation disparity. Jefferies analyst John Hecht and Mizuho researcher Dan Dolev both have a $12 price target for SoFi — implying about 60% upside from the current price. Andrew Jeffrey of Truist Securities is slightly more bullish, calling for about 90% upside with his $14 price target.

While I can’t predict how high SoFi shares may rise, I’m confident in calling the stock dirt cheap at its current price. I think a lot of investors misunderstand SoFi’s business, and do not appreciate how much progress the company has made in just a few short years.

It’s intriguing to see more analysts on Wall Street turn bullish on SoFi’s prospects as well. With an accelerated top line and consistent profits on the horizon, I think now is a terrific opportunity to use dollar-cost averaging to initiate or add to an existing position in SoFi and hold for the long term.

Charles Schwab is an advertising partner of The Ascent, a Motley Fool company. Wells Fargo is an advertising partner of The Ascent, a Motley Fool company. Bank of America is an advertising partner of The Ascent, a Motley Fool company. Adam Spatacco has positions in Block and SoFi Technologies. The Motley Fool has positions in and recommends Bank of America, Block, Charles Schwab, Jefferies Financial Group, PayPal, Truist Financial, and Upstart. The Motley Fool recommends the following options: short June 2024 $65 puts on Charles Schwab and short June 2024 $67.50 calls on PayPal. The Motley Fool has a disclosure policy.

: Robinhood acquires Bitstamp in a 0m deal")