This Is Hands-Down My Pick for the Best Artificial Intelligence Stock to Buy Now. (And It’s Not Nvidia.)

")

The “Magnificent Seven” stocks might garner most of the attention in AI, but there are plenty of other emerging opportunities.

The market is off to a sizzling start so far in 2024, with the S&P 500 and Nasdaq Composite trading near record levels, and perhaps the biggest influence right now is artificial intelligence (AI).

The tech stalwarts in the “Magnificent Seven” are indeed making waves in AI and constantly find their names in the spotlight. But outside of big tech, there are other disruptive forces in AI. Palantir Technologies (PLTR -3.12%) is one such player, with various AI-powered enterprise software platforms for the public and private sectors.

Last year was a milestone for Palantir, and I think the best is yet to come. Here’s why it’s my top pick for investors in a highly contested AI arena.

Customer acquisition is rising

Several big tech companies have partnered with leading AI start-ups. For example, Microsoft has invested billions into OpenAI, the developer of ChatGPT. Amazon and Alphabet are both investors in OpenAI competitor Anthropic and Nvidia is an investor in Databricks.

Palantir has figured out a way to make inroads in this AI landscape. A year ago, the company released the Palantir Artificial Intelligence Platform (AIP).

To fend off the competition, the company began hosting seminars called “boot camps,” where prospective customers could demo its AIP software. The goal was to help potential customers identify a use for it.

This lead-generating strategy appears to be working. In 2023, Palantir increased its customer count by 35% year over year. Moreover, the company is accelerating its expansion beyond its legacy government-contractor business.

It grew its private-sector customer count by 44% last year. In the fourth quarter, U.S. revenue from these clients grew 70% year over year.

Image source: Getty Images.

Revenue, margins, and profits are up

Looking at the company’s finances sheds some light on how AIP is helping Palantir. The company was founded in 2003 and took 17 years to reach $1 billion in revenue. Just three years later, it eclipsed $2 billion in sales.

In 2023, Palantir’s revenue increased 17% year over year to $2.2 billion, underlining how quickly breakthroughs in AI are unlocking new growth for software companies.

Even better, the company is witnessing a surge on the bottom line as well. Last year, free cash flow grew more than threefold to $730 million, and operating margin expanded 6 percentage points year over year.

The best is yet to come

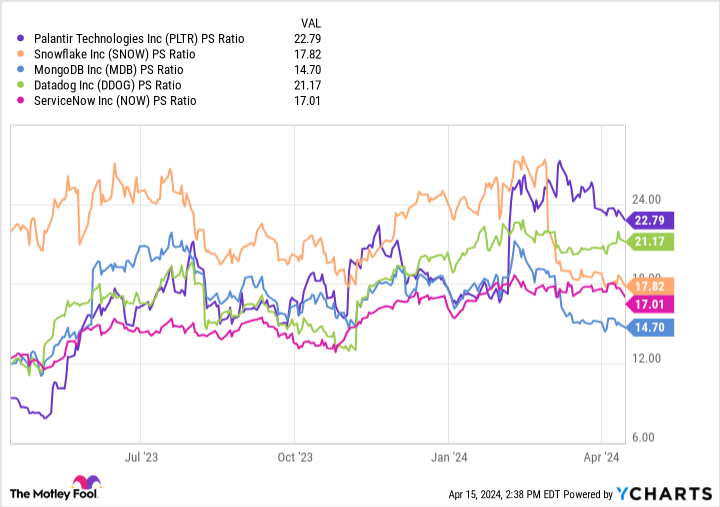

The chart below benchmarks Palantir against peer high-growth software-as-a-service (SaaS) developers in AI. The company’s price-to-sales (P/S) ratio of 23 is the highest among this cohort, narrowly above Datadog.

While the stock has become a little pricey, it’s important to note that Palantir’s valuation multiples really began to expand in February following the company’s strong fourth-quarter earnings report. Since that report, optimistic buying activity has fueled newfound momentum in the share price.

PLTR PS ratio data by YCharts.

Despite its premium price, Palantir stock still looks attractive to me. It is trading 43% below its all-time high.

Moreover, one of Wall Street’s most esteemed technology analysts, Dan Ives of Wedbush Securities, is calling for massive upside in the stock. He set a price target of $35, nearly 59% above current trading levels. Analysts don’t always get things right, but I’m in agreement with Ives’ optimism.

My take is that Palantir is well worth the premium. The combination of top-line growth and robust cash flow makes it stick out among the competition because many high-growth SaaS businesses are not yet consistently profitable. In Q4, Palantir reported its fifth consecuve quarter of GAAP (unadjusted) profitability.

Furthermore, the financial and operating results mentioned above drive home the idea that the company’s decades of investing in AI provide a competitive advantage. This has led to a new wave of growth, with consistently strong sales and profits.

The progress to date is encouraging, but I think Palantir’s long-term journey to disrupt big tech is just getting started. Now looks like a lucrative opportunity to use dollar-cost averaging to help build a position or add to an existing one. Investors with long time horizons won’t want to miss out on the company’s potential in AI.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Microsoft, Nvidia, and Palantir Technologies. The Motley Fool has positions in and recommends Alphabet, Amazon, Datadog, Microsoft, MongoDB, Nvidia, Palantir Technologies, ServiceNow, and Snowflake. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.