Unveiling Salesforce (CRM)’s Market Position: A Comprehensive Va

’s Market Position: A Comprehensive Va")

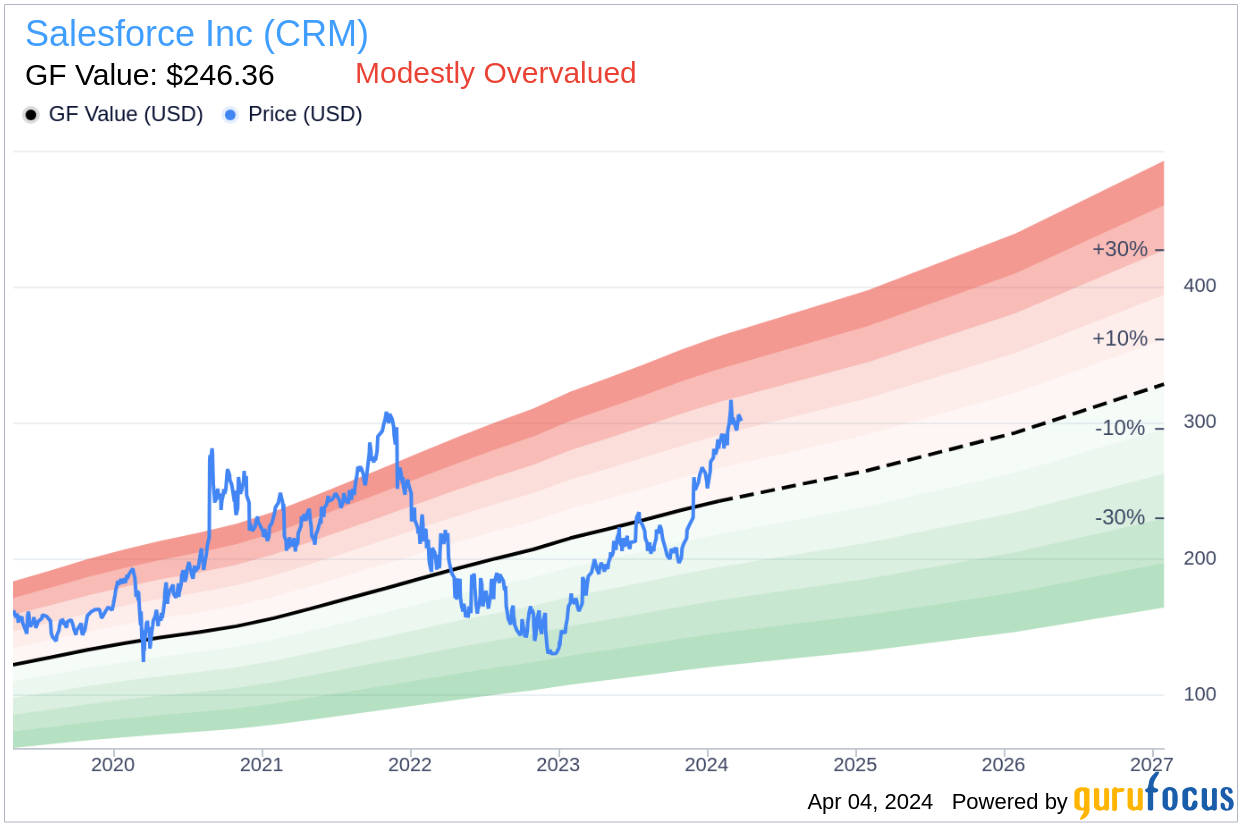

Salesforce Inc (CRM, Financial) experienced a daily loss of -1.88%, yet it has gained 17.17% over the past three months. With an Earnings Per Share (EPS) of 4.2, investors may wonder if the current market valuation accurately reflects the company’s intrinsic value. Is Salesforce modestly overvalued? The following analysis aims to shed light on this question and provide investors with a clearer picture of Salesforce’s fair market value.

Company Introduction

Salesforce Inc provides comprehensive enterprise cloud computing solutions, with a focus on customer relationship management. The company’s Customer 360 platform is designed to unify customer data across various systems, apps, and devices, facilitating enhanced sales, customer service, marketing, and commerce operations. With a suite of services including Service Cloud, Marketing Cloud, Commerce Cloud, and more, Salesforce is a key player in the cloud technology space. Currently, the stock price stands at $299.01, with a market cap of $290 billion, posing the question of how this compares to the GF Value’s fair valuation estimate.

Understanding GF Value

The GF Value is a proprietary metric used to determine the intrinsic value of a stock. It incorporates historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and projected future business performance. The GF Value Line serves as a benchmark for the stock’s ideal fair trading value.

Salesforce’s current price suggests that it may be modestly overvalued. The GF Value estimation, which takes into account historical multiples, an internal adjustment based on the company’s past growth, and future business performance expectations, indicates that stocks trading significantly above the GF Value Line could yield poorer future returns. Conversely, those below the line could offer higher returns. Salesforce’s market cap of $290 billion further illustrates its position in the market relative to its intrinsic value.

Given Salesforce’s relative overvaluation, its stock’s long-term return could potentially lag behind its business growth, warranting a cautious approach for value investors.

Link: These companies may deliver higher future returns at reduced risk.

Financial Strength Assessment

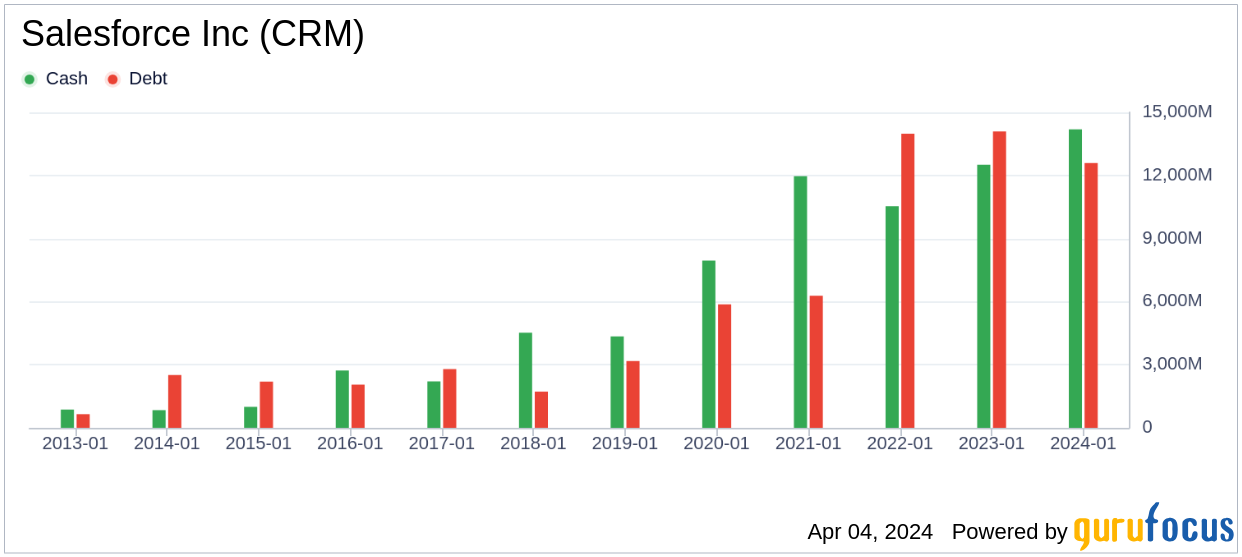

Investing in companies with robust financial strength is crucial to mitigate the risk of permanent capital loss. Important indicators such as the cash-to-debt ratio and interest coverage can provide insights into a company’s financial resilience. Salesforce’s cash-to-debt ratio stands at 1.13, which is less than ideal when compared to peers in the Software industry. However, its overall financial strength is considered fair with a score of 7 out of 10.

Profitability and Growth Prospects

Profitable companies, especially those with a history of consistent earnings, generally present lower investment risks. Salesforce, with profitable operations in 8 out of the past 10 years, demonstrates strong profitability. The company’s operating margin of 17.21% outperforms 85.88% of its industry counterparts. With a revenue of $34.90 billion and an Earnings Per Share (EPS) of $4.2, Salesforce’s profitability rank is a robust 8 out of 10.

Regarding growth, Salesforce’s 3-year average annual revenue growth of 15.7% is commendable, surpassing 66.53% of industry competitors. Its EBITDA growth rate of 41.8% is even more impressive, ranking higher than 85.5% of companies in the Software industry. Such growth is indicative of potential value creation for shareholders.

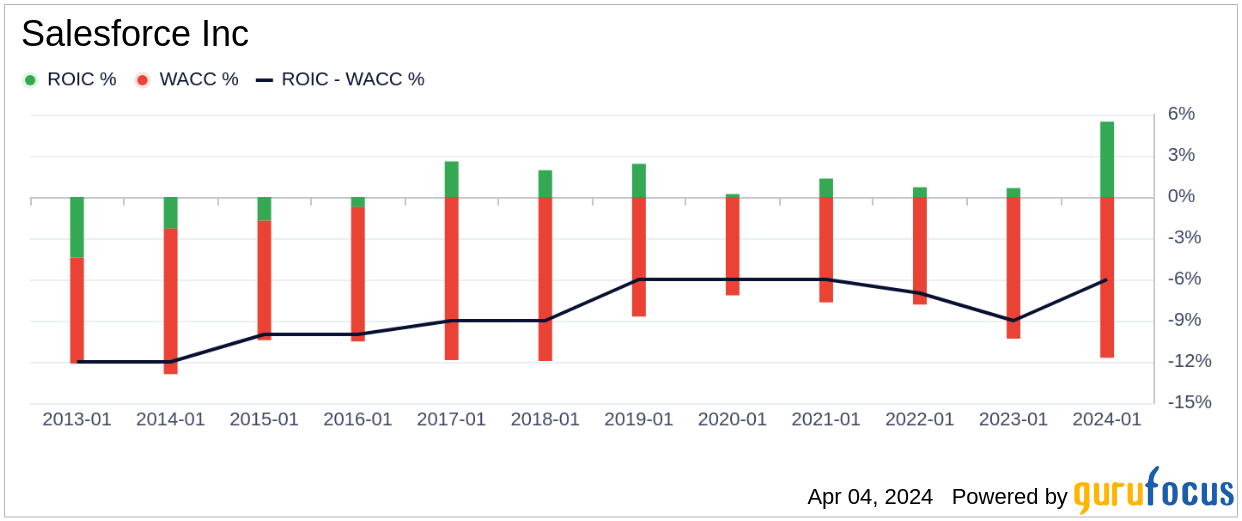

ROIC vs WACC: Measuring Profitability

The comparison between a company’s Return on Invested Capital (ROIC) and its Weighted Average Cost of Capital (WACC) is a key indicator of profitability. Ideally, ROIC should exceed WACC to indicate efficient capital utilization. Salesforce’s ROIC is currently 5.67, which is below its WACC of 12.23, suggesting room for improvement in capital efficiency.

Conclusion

Overall, Salesforce (CRM, Financial) appears modestly overvalued. Despite this, the company maintains fair financial condition and strong profitability, with growth rates that outshine a significant portion of the Software industry. For a deeper understanding of Salesforce’s financials, investors can explore its 30-Year Financials here.

To discover high-quality companies that may offer above-average returns, consider using the GuruFocus High Quality Low Capex Screener.

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.