What Gen Z want from UK fintech

As the digital era of financial services progresses, the UK fintech sector has reached new and diverse audiences that have varying demands from their financial providers. Gen Z is a significant demographic that are currently entering or are in the workforce,

and having been raised in a more virtual and digitalised environment, expect ease, speed, and consistency from their payments providers.

This is an extract from the recently published report, ‘The Future of UK Fintech – 2015-2035’.

According to McKinsey, a large proportion of Gen Z are experiencing financial nihilism – due to the current economic situation, geopolitical state, and cost of living crisis leading to lower salaries and higher prices, almost 25% of Gen Z do not expect to

retire. Therefore, the generation has a strong commitment to holding their banks to an ethical standard, managing their savings, and having multiple bank accounts to manage their funds to the best of their ability.

What do younger users demand from their payments providers?

The new generation of fintech consumers expect real-time responses, constant accessibility, and hyper-personalised services from their financial services. Instant gratification and frictionless experiences are the future.

Zopa Bank’s chief customer officer, Clare Gambardella stated: “These consumers have grown up with digital banking apps and instant payments as the norm and are looking beyond that, for banks which truly simplify their experience of managing their finances.

Fintech consumers have also often experienced a lot of change to their economic circumstances in recent years. They expect great value from their banking products and want to take charge of their financial destiny.”

It is not shocking that 99% of Gen Z and 98% of millennials manage use mobile banking apps for most of their financial needs. Challenger banks that a digitally native are popular among the younger crowd in offering a suite of features that includes investment,

budgeting, and payment tools within one app. Revolut, Starling, and Monzo are particularly popular for Gen Z in the UK due to their user-friendly interfaces and easy access to features.

Statistics from GW Solutions recorded in February 2024 found that Monzo has 4.2 million monthly active users in the UK, making it the 7th more popular mobile banking app and most popular digital bank. Yet, Monzo’s monthly users are falling year-on-year.

Starling currently has 2.4 million monthly active users in the UK.

Both Starling and Monzo have a strong user base of 18-34 year olds, with 39% and 44% respectively. This compares to the most popular banking app in the UK, Halifax, which has only 24% of users within that age bracket. The research found that Barclays and

Lloyds had to the most balanced age distribution, with at least 20% of users in each age group.

Additionally, 30% of bank app users have accounts with more than one bank, with the top 5 UK banks with the most overlap being Chase UK (70%), first direct (59%), Monzo (54%), Starling (53%), and TSB (51%).

These numbers indicate that users are experimenting with multiple banks, and that younger mobile app users are more inclined to hold bank accounts in digital-only banks, alongside having a bank account with a larger, more traditional bank.

Chief revenue officer at Marqeta, Todd Pollak detailed the demands of the new generation: “Digital native generations are unlikely to engage with physical cards and bank branches in the same way that past generations did, and instead, are looking for financial

products that can interact effectively with their digital, fast paced lives.”

A variety of features within digital wallets and banking apps also appeal to younger, tech-savvy consumers outlines Gurdeep Singh Kohli, member of SC Ventures. He stated that younger users seek for embedded financial education within apps and incentives

for spending, and that features such as family financial management that tracks saving and spending are also untapped opportunities.

Gambardella, pointed out that new consumers often have multiple bank accounts and credit cards, revealing that customers are more likely to “shop around” for products to find the right fit. The younger, digital-savvy age of fintech consumers have higher

expectation of their financial providers to be able to give them the services they need quickly, efficiently, and seamlessly. As seen in the graph below, the most popular digital banking apps also have the lowest average time for a payment notification to

appear.

Pollak concluded: “Younger generations’ buying power, already strong, will only grow as they age into their highest-earning years. Gen Z have higher expectations for companies they do business with, and are more likely to turn to another brand following

issues with quality of perceived lack of authenticity and social responsibility. This has had an impact on the financial market as well, with only 27% of GenZers citing they are very satisfied with their credit card and 58% citing they are likely to apply

for a new credit card in the next 12 months. With Gen Z shifting the narrative of brand loyalty, companies need to revisit their traditional loyalty approaches, which are largely based on legacy, long standing credit card programmes , to attract and retain

Gen Z customers.”

Source: Built of Mars

Gen Z drive sustainable payments

Sustainability has become a tenet of the financial services world in recent years, in part due to younger users’ commitment to working with companies that maintain sustainable values and pursue greener initiatives.

64% of Gen Z would switch banks if their current account holder did not hold up their standards for ethics and environmental sustainability. Gen Z’s has shown that they have the willpower to only work with companies whose values align with their own, and

have proven so again and again through the usage of environmentally-conscious payments services.

Emma Kisby, Cogo CEO, EMEA, stated that Gen Z and millennials make up a third of their engaged users for carbon footprint technology, indicating how invested the younger generation is in maintaining sustainable principles and looking for responsible and

trustworthy institutions to put their money into. More and more banks and fintech are seeing how younger generations have an enthusiastic response to corporate accountability and transparency, as they are looking to invest in businesses that reflect their

own values.

Kisby stated: “It’s well known that young people are worried about climate change and its effects, so it makes sense that fintech addresses these concerns. We’ve seen from our own research at Cogo that 71% of people under 25 want their banks to support their

sustainability journey and 71% of customers want their banks to offer rewards and incentives to encourage more sustainable purchasing decisions. People under 25 (79%) are particularly supportive of this incentive.”

New forms of engaging with financial services

After experiencing the pandemic and many experiencing financial upheavals and debt, Gen Z is more mindful when it comes to saving, avoiding debt, and managing credit. However, Investopedia reports that Gen Z is concerned about managing risk and accumulating

mortgage and personal loan debt.

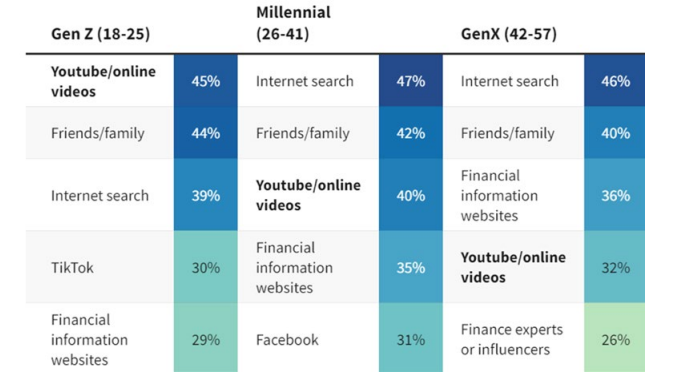

Pollak stated that Gen Z are engaging with merchants in new ways, using new services such as BNPL to avoid debt and looking to flexible credit options. Pollak added that Gen Z are actively interested in their financial independence and seek to learn about

personal finance on TikTok and YouTube. As seen in the graph below, Gen Z learn most about persona finance from online videos than millennials and Gen X.

Source:

Investopedia

‘Finfluencers’ are becoming more common online on YouTube and FinTok (Finance TikTok), who post personal finance content and advice to viewers. From investment tips to explaining the stock market and crypto, FinTok creators are gaining traction with young

investors who are looking to become fiscally responsible.

Mark Horwood-James, managing director of personal finance technology at Moneyhub, commented on Gen Z’s usage of social media for financial tips: “The research has shown that social media is one of the most popular sources for financial tips and advice among

that group. The challenge is that this ‘advice’ is unregulated, which makes it hard for consumers to discern whether the information is accurate or unbiased. Firms need to embrace innovation and technology and deliver financial content to younger generations

in ways that are convenient and helpful to them across various mediums and formats.”

Personal finance tools that can be used in apps such as Starling track user spending habits and can act as a financial advisor, which appeals to the younger generation who are hungry for data on their spending habits to manage their funds.

McKinsey reported that over half of Gen Z have some kind of investment, and that Gen Z holds the biggest share of fintech users.

Pollak commented: “Contrary to common stereotypes, Gen Z exhibits a high level of fiscal responsibility and aversion to debt, as a result, their relationship with credit is continuously evolving.”

Gen Z will revolutionise financial services

In recent years the financial services and banking sector has experienced a golden age of innovation and drastically charged into the digital economy.

Currently, Gen Z is on the rise in changing the financial sector for the better, demanding companies take accountability for their impact on the environment and reduce their carbon emissions, and looking for banks that reflect their ethical values. Additionally,

younger users demand hyperpersonalisation and speed from their payments providers, expecting seamless and user-friendly interfaces.

Gen Z is not afraid to jump between accounts, moving between incumbents, fintechs, and challenger banks to get what they need. As Gen Z continue to grow and become more dominant in their financial habits, their demands will continue to define the trends

of the sector.